Texas’ economic outlook for 2012 is positive, with job growth occurring in several sectors and low cost of living enticing businesses to move here. It will be tougher going for the nation, however, because the housing market needs to clear a huge number of foreclosures, consumers need to pay off their debt, the banking system needs to write off bad debt, and small businesses need to start hiring again.

Jan 23, 2012

Texas Sails On: Nation Battles Headwinds

This year (2012) looks to be a better one for Texas’ economy, but the United States as a whole is still attempting to overcome serious obstacles to recovery.

The new year is upon us. Business owners, investors and households are trying to anticipate what the economy will look like in the months ahead.

While there are no doctoral degrees in clairvoyance or fortune telling, it’s not difficult to understand why weather forecasters and economists would be interested in acquiring those skills. Both professions have one thing in common: hundreds of variables interact to create changes in the weather and in the economy. When most of these variables are stable and predictable, forecasting is rather easy. But when they are in a frenzied state, forecasting the outcome of their interaction becomes challenging. Ultimately, weather forecasters and economists attempt to discern patterns out of chaotic data.

Leading Indicators Suggest Direction

Economic indices of leading indicators were created specifically for the purpose of anticipating future business activity. The Leading Index for the United States (Figure 1) is just such a measure. The index is hinting at modest positive economic growth in the next 12 months. It has been oscillating between 200 and 400 for most of 2011, which is about where it was from 2003 through 2006, when the economy was expanding at a modest clip. The current level is slightly less than in the late 1990s when the economy was expanding much more rapidly.

The Texas Index of Leading Indicators (Figure 2) shows a much more robust economic outlook for 2012 compared with the national economy. The Center’s Monthly Review of the Texas Economy documented how Texas dramatically outperformed the United States in 2011, with positive job growth not only in the energy industry, but also in construction, manufacturing, retail, transportation, professional business services, health care and hospitality. Only the government sector and the information industry declined.

Texas has a lower cost of living and a lower wage structure than many states. This allows Texas businesses to be more competitive in the global market and keep jobs in America. For example, General Electric recently announced it will build a $95 million mining equipment plant in Fort Worth to build electric drive systems for huge off-road vehicles. In the current economic environment, this is a huge accomplishment.

The Texas Index is currently in the range of 120 to 123, similar to that of 2004–05, when the previous economic recovery occurred. Job growth is occurring in nearly all Texas metro areas and is likely to continue into 2012, albeit at a modest pace.

Over 11 million people in Texas have jobs. This number is higher than it was in 2008 when the recession started. The state has fully recovered all the jobs lost during the recession. By comparison, for many states, full recovery could be years away.

Problems Yet to Solve

If this was a typical recession, we would expect the U.S. economy to expand at a faster rate after three years of decline. Unfortunately, this is not a typical recession.

Four key drags to the economy haven’t yet been remedied.

First, we haven’t seen the normal rebound in housing construction that typically leads the economy out of recession. Normally, a recession brings lower interest rates, which make housing look attractive, so people start to buy and build homes. So far, that hasn’t happened. Residential construction has virtually collapsed and shows no sign of rebounding (Figure 3).

Several things have to happen before significant increases in housing construction will occur. First, somewhere between 4.5 and 6 million more foreclosures need to occur. Until this happens, people will be skittish about buying, fearing a price decline when these homes are sold. The foreclosure process is scaling up, but the Office of the Comptroller of the Currency estimates it could take 50 months to move these homes back into the hands of homeowners or investors.

Again, Texas is an exception. Foreclosure activity is much lower here than in other parts of the country.

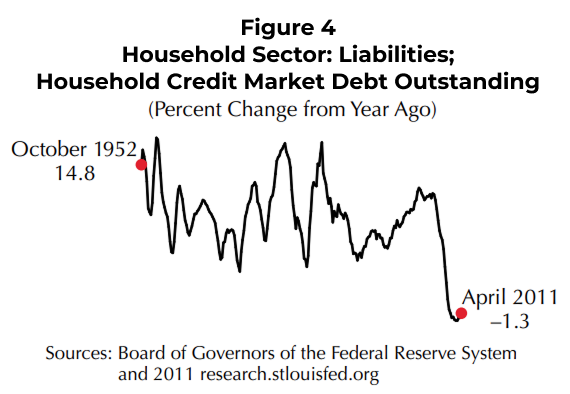

The second headwind slowing recovery is that Americans have borrowed too much in the past five years and now they have to pay it back (Figure 4). Sixty-five to 70 percent of the U.S. economy is based on consumer spending. When credit increases, people spend more. When credit contracts, they spend less.

Until credit starts to expand again, economic growth will be subdued. Outstanding credit in America has never declined in the past 60 years, until just recently. This is why the U.S. economy will experience only modest job growth for the next several years.

Until Americans get their debt levels down to manageable levels, they will save more and spend less.

The third headwind is that the banking system is still struggling with solvency. While banks have written off some bad debt, significant losses have yet to be recognized. First mortgage loan losses and losses on second mortgages and home equity lines of credit will have to be dealt with in the future. Until this process is completed, the U.S. banking system will limp along, with many bankers and bank regulators extremely averse to taking on risk with new loans.

In Texas, banks appear to be much stronger than their cousins in other states. However, Texas banks are subject to regulation by the same people who regulate banks all over the country. And those regulators are not encouraging loan expansion at this point.

The fourth headwind to a more rapidly growing economy is that small business owners in America are still reluctant to hire (Figure 5). Even though profits are good, cash flow is good and $2 trillion in cash is sitting on their balance sheets, they are so baffled by the current economy and regulatory environment that they aren’t yet interested in hiring. This is the key to the U.S. economy’s rebound. Businesses must begin to hire again. The monthly survey from the National Federation of Independent Businesses, which represents small business owners, shows that the number of business owners who say they are going to hire in the next six months has been hovering around zero for the past three years.

Can Congress create an environment that will encourage businesses to begin to expand and hire again? If they do, the American economy will hum with enthusiasm.

In the meantime, the U.S. economy is likely to struggle to generate jobs again in 2012, because so many important issues that powerfully impact business owners and investors will not get resolved until after the 2012 election.

Because of the pent-up demand from businesses and investors and families who have been postponing economic decisions for three years now, the economy appears to be “spring loaded.”

Fortunately, Texas is poised to outperform the U.S. averages. Home sales volume in Texas should show modest improvement over 2011, and prices should be stable throughout 2012.

Americans do not tolerate deferred gratification for very long. We have dreams and we want to live them out. Once the federal government creates a positive environment for business owners, we might be pleasantly surprised at the vigor of the recovery.

Dr. Dotzour ([email protected]) is chief economist with the Real Estate Center at Texas A&M University.

Did you like this Article?