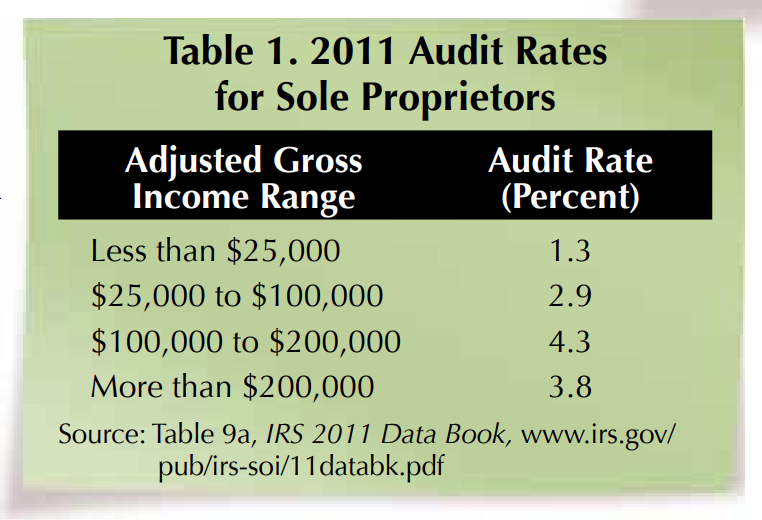

Depending on income level, 2011 IRS audit rates on small businesses, which include most real estate professionals, ranged from 1.3 to 4.3 percent. Audits increased tax liabilities between $8,000 and $18,000 in most cases.

Jan 9, 2013

The Tax Auditor Cometh

Internal Revenue Service statistics show that 1.3 to 4.3 percent of small businesses and sole proprietorships were audited in 2011, compared with less than 1 percent of individuals. That puts most real estate professionals squarely in the IRS’ sights.

Early last year, the IRS released its 2011 Data Book, which provides data on its audit activities, tax collections and related projects. Overall, the IRS audited slightly more than 1 percent of approximately 143 million individual 2010 tax returns.

While the overall audit rate was slightly more than 1 percent, the rate varied by adjusted gross income (AGI; gross income less losses and certain business deductions). Audit rates for AGI levels between $1 and $200,000 were just under 1 percent. In sharp contrast, the rate for AGIs from $200,000 to $5 million ranged from 3 to 12 percent. The rates for AGIs over $5 million averaged 21 to 30 percent.

While audit rates seem low for the majority of taxpayers, keep in mind that the rates are averages. The probability of audit can be much higher depending on the size and type of income and deductions as well as how the tax return compares with all others in that category.

For example, IRS 2011 audit rates on small businesses/sole proprietorships ranged from 1.3 to 4.3 percent depending on income level. These relatively higher rates directly affect real estate professionals, who are generally considered self-employed (and, therefore, sole proprietors) for tax purposes (Table 1).

During 2011, the IRS audited 278,000 sole proprietorship returns. This total was 18 percent of all audited returns filed by individuals.

Audit statistics for sole proprietorships strongly imply that the IRS believes small-business owners underreport income, overreport deductions or both. Approximately 75 percent of audits in the $25,000 to $100,000 category resulted in assessed tax increases averaging $8,000. For the $100,000 to $200,000 income category, an average $18,000 additional tax was assessed on 69 percent of audited returns.

In addition to assessed tax increases, interest and (sometimes) penalties are levied. Taxpayers have the option to appeal assessed amounts through the IRS administrative appeals system and, ultimately, the courts.

All taxpayers are allowed to deduct legitimate expenses. If audited, however, taxpayers must provide proper documentation. For real estate professionals, documentation is necessary for business meals, auto expenses, travel, entertainment, home offices, and, in some cases, the number of hours devoted to property management.

The main audit selection procedures include “programs” targeting specific groups; tax returns with atypical relationships between income and deductions; or a combination of both. The combination approach probably explains the higher audit rates for the self-employed. Specifics of actual audit selection processes are not made public.

Audits associated with atypical income-deduction relationships are, in part, determined by the IRS statistical discriminant inventory function (DIF) system. This method scores each tax return with a DIF score. Returns with the highest DIF scores are reviewed by IRS staff to determine if an audit seems necessary. The discriminant function equations are a closely guarded IRS secret.

While DIF system details are not publicized, the IRS does release average itemized deduction amounts for various AGI levels. Table 2 indicates averages based on 2009 tax returns (the most recent year for which data are available). Taxpayers can compare their own itemized deductions to the averages.

As noted, taxpayers should deduct all legitimate expenses for which they have documentation. Assistance from a competent tax accountant or tax attorney is advised.

Dr. Stern ([email protected]) is a research fellow with the Real Estate Center at Texas A&M University and a professor of accounting in the Kelley School of Business at Indiana University.

Did you like this Article?