While no method exists to predict housing bubbles with certainty, the relationship between home prices and economic fundamentals such as supply and demand can offer insight into bubble formation. Basically, when price expectations exceed actual outcomes, and when people believe that prices will continue to increase indiscriminately in the future, warning lights should come on.

Jan 7, 2014

Bubble Vision

Asset price bubbles, including the housing bubble that wreaked havoc in the early 2000s, are hard to predict. Economists can, however, get some insight into bubble formation by studying the relationship between home prices and economic fundamentals such as supply and demand.

House prices in the United States increased dramatically during the pre-2007 housing boom. Many economists and policymakers argued that a bubble did not exist and that numerous fundamental factors — job and income growth, low mortgage rates, demographics and restricted supply — were behind the price increases, making a substantial nationwide decline in house prices improbable.

But overly optimistic expectations about future price growth, along with government policies, led to a relaxation in lending standards. This resulted in a housing bubble. In regions where housing prices registered the highest increases, past price performance had a significant influence on subsequent loan approval rates. When price expectations did not materialize, the bubble burst, setting off a chain of events that led to a global financial and economic crisis comparable only to the Great Depression of the 1930s.

Like stock prices, house prices have boom and bust cycles because market participants tend to expect higher future returns when prices are high relative to fundamentals. “Irrational exuberance” comes into play when buyers and sellers in the midst of a bubble expect high future returns because they extrapolate recent price behavior into the future. This is fueled further by buyers’ perception that housing investment entails little risk of price declines.

About Housing Bubbles

Bubbles have occurred throughout history in many countries and various asset markets. In the case of real estate markets, the widespread use of the term “housing bubble” is relatively new. It wasn’t until 2000 that the term “housing bubble” appeared in the media as speculation mounted of a bubble forming. Bubbles can be defined as market participants’ expectations of high future prices that are not aligned with economic fundamentals but are instead based on recent trends of high-growth performance. This requires that market participants be able to finance their inordinate asset purchases.

The concept of a bubble is based on the public’s: (1) expectations that prices will continue to increase; (2) theories about the risk of falling prices; and (3) worries about being priced out of the future housing market if they don’t buy today. During a housing price bubble, homebuyers’ ideas about affordability are distorted; a home once considered too expensive is now seen as an acceptable purchase. Furthermore, they perceive little risk in purchasing a home because they consider a fall in housing prices unlikely.

Bubble Trouble

So why wasn’t the housing bubble identified and subsequently avoided?

The problem with bubbles is that they cannot be identified with any certainty or confidence. If they could be, they would never form in the first place. Instead, the market would respond by selling assets to avoid future losses rather than purchasing homes at high prices. Identifying the beginning of a bubble requires extraordinary insight into the functioning of a market that even highly knowledgeable and specialized market participants lack.

Despite the difficulties in determining the existence of bubbles, economic fundamentals can help detect them. This is especially true in the housing market, where the underlying fundamentals of supply and demand can be used.

Housing as Investment Asset

Market participants’ widespread inclination to view housing as an investment asset is a defining characteristic of a housing bubble. Speculation in housing investment is a factor in the creation of bubbles and also contributes to their instability as the investment motive weakens. When the attractiveness of housing as an investment deteriorates due to a fear of price declines, the bubble can burst.

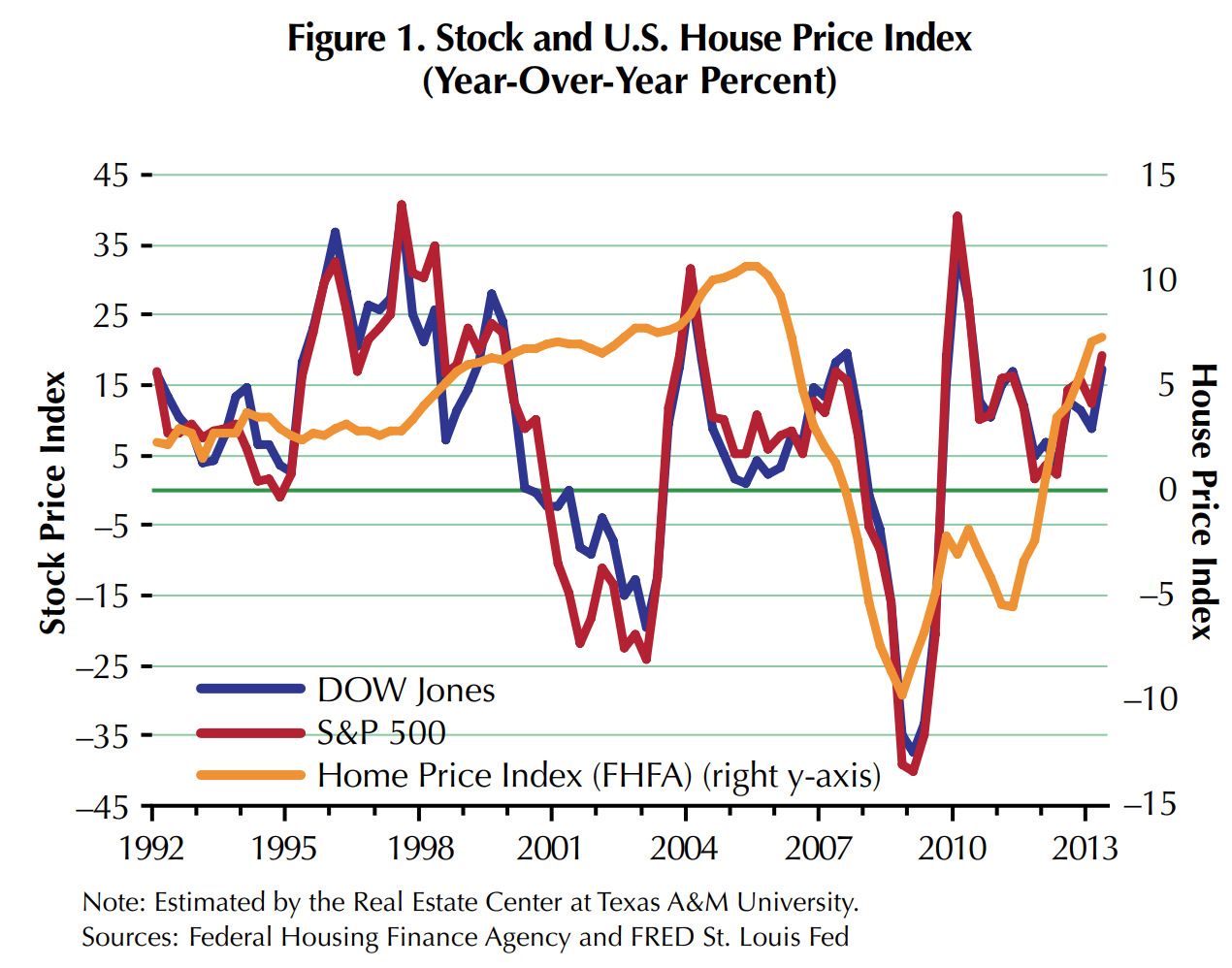

Even after the Great Recession, homeowners continue to perceive housing as a stable investment relative to the stock market given that declines in nominal house prices are rare compared with stock prices (Figure 1). This important difference between housing markets and stock markets, as well as most asset markets, is based on the fact that home prices are “sticky downward.” That is, when excess supply occurs, prices do not immediately fall, allowing the market to find a new equilibrium and clear. Rather, sellers have “reserve” prices that they are not willing to go below.

The investment motive for purchasing a home is said to play an important role in housing bubbles. Popular misconceptions about housing investment include:

- bubbles cannot form in single-family residential real estate;

- single-family residential real estate is an investment that cannot lose money;

- single-family residential real estate is a candidate for the “best investment” that can be made;

- high-priced housing (such as a beach house) typically has higher price rate increases than other properties perceived as less valuable;

- when housing is in short supply, home prices become irrelevant and can increase indiscriminately; and

- when selling prices are higher than list prices, economic fundamentals determining supply and demand are no longer valid, and home prices can increase continuously

Housing Market Fundamentals

Housing prices are determined by supply and demand. On the demand side are factors such as demographics, income growth, employment growth, changes in financing mechanisms or interest rates, and changes in tastes and preferences based on locational characteristics, such as accessibility, schools or crime. For example, a household’s income could increase, allowing it to purchase a home; a large proportion of the population could be forming new households; or mortgage rates could have fallen.

Supply side factors include construction costs (lumber, drywall, labor), interest rates, housing stock age, building technology and land availability. Elasticity of supply is a key factor in the cyclical behavior of home prices.

If the supply of homes is elastic, any small change in housing prices can be matched by an increase in supply. Indeed, if demand for housing puts upward pressure on home prices, the quantity of new homes built can be increased to satisfy demand. In the process, the pressure on home prices to continue to rise is eliminated.

When home price increases are not based on changes in the economic fundamentals that determine underlying supply and demand, a bubble exists, increasing the possibility that housing prices could suddenly collapse as market participants realize their home price expectations will not be met.

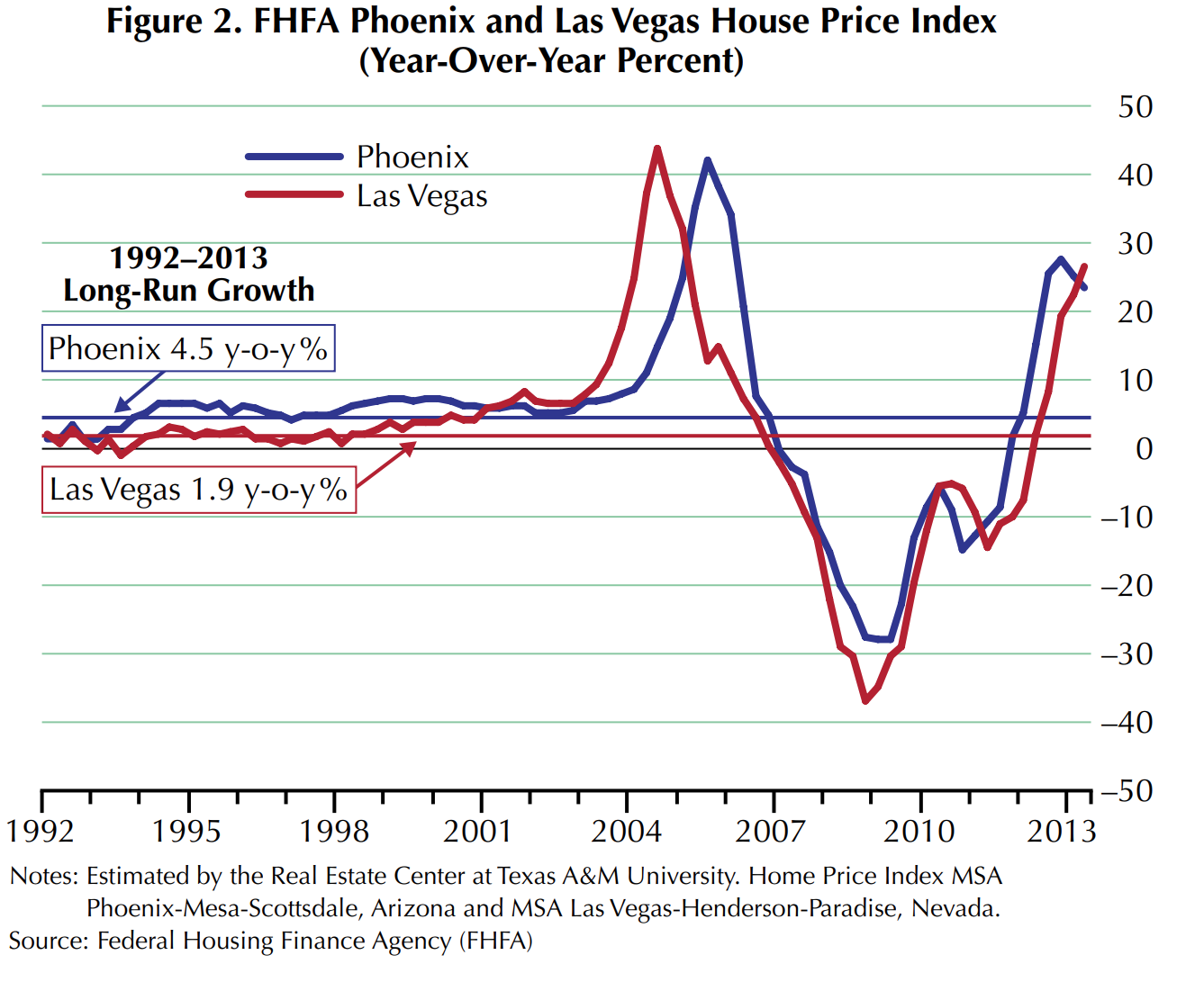

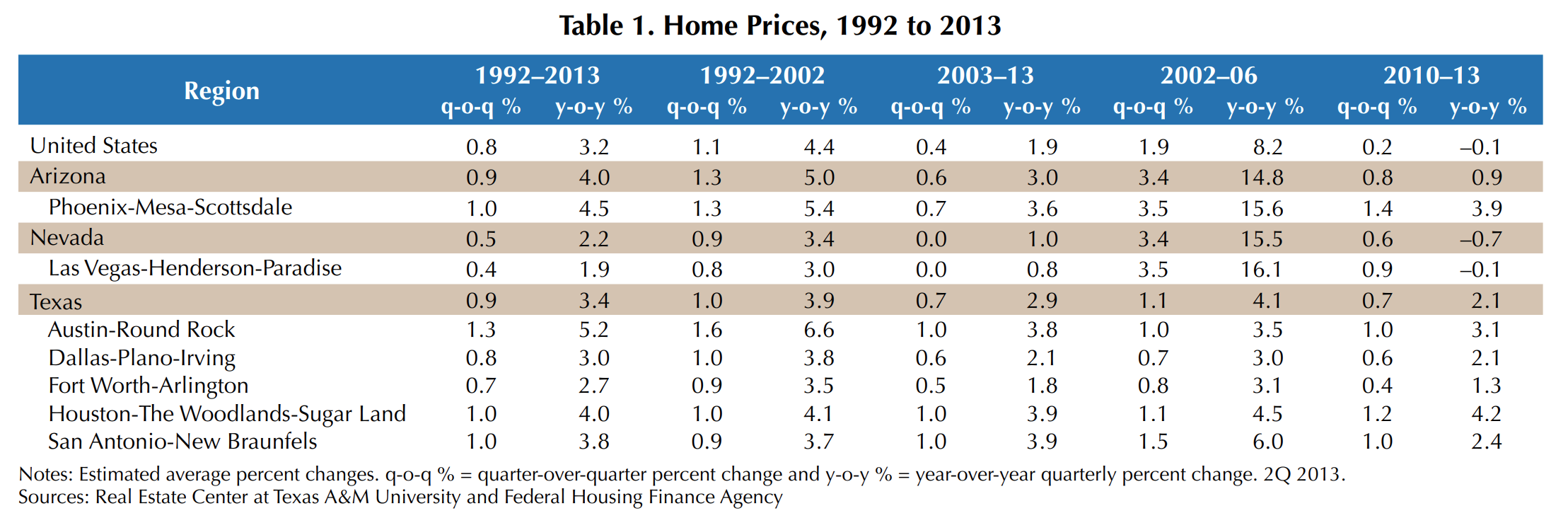

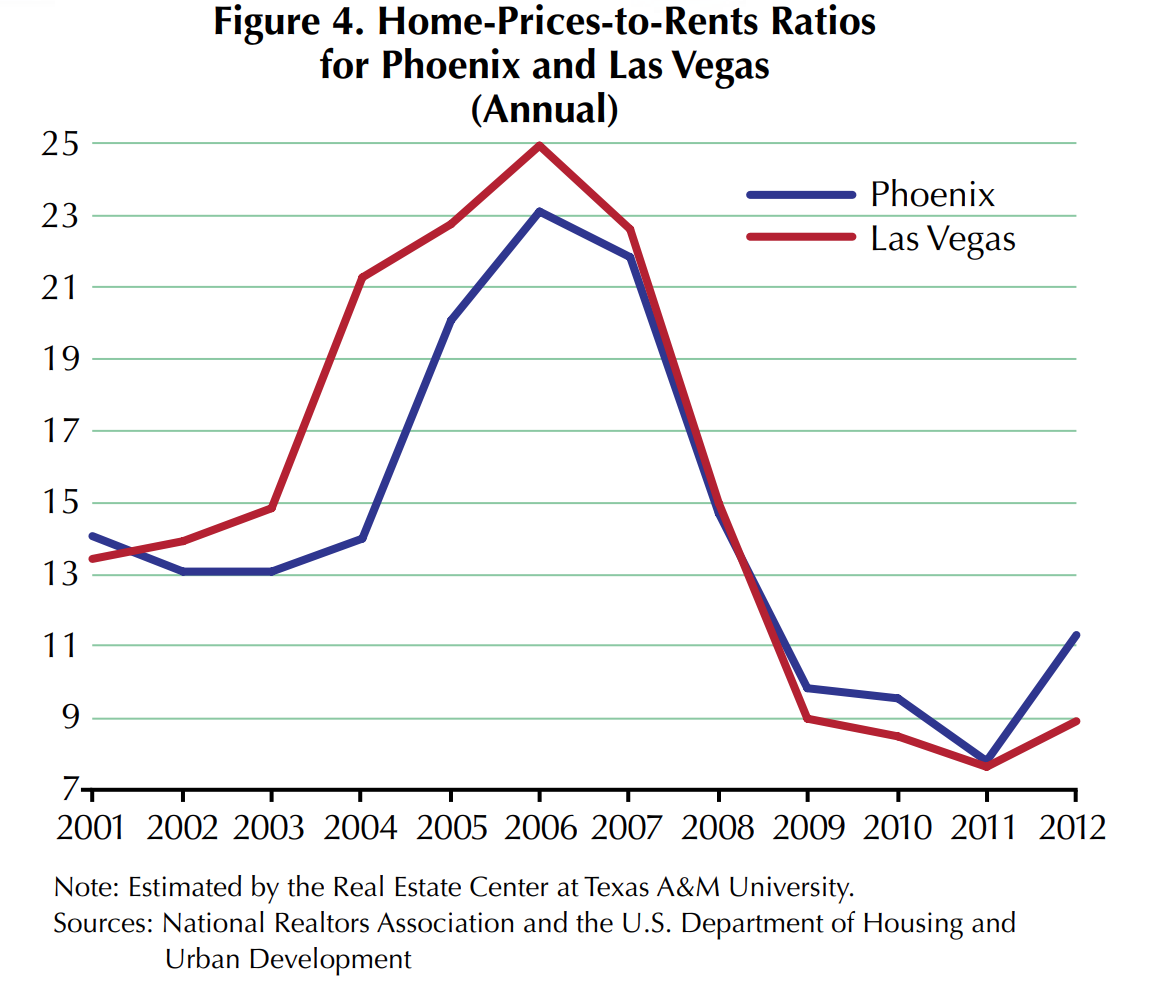

A rapid increase in prices doesn’t necessarily imply a bubble. It is, however, a good indicator that price increases may not be based on economic fundamentals, especially if price increases for that region do not reflect overall historical price trends. This was evident in Phoenix and Las Vegas where home prices from 2002 to 2006 grew at extraordinarily high rates versus historical price increases for those regions (Figure 2). During that period, home prices in the United States also registered a higher rate of growth than previously observed (Table 1).

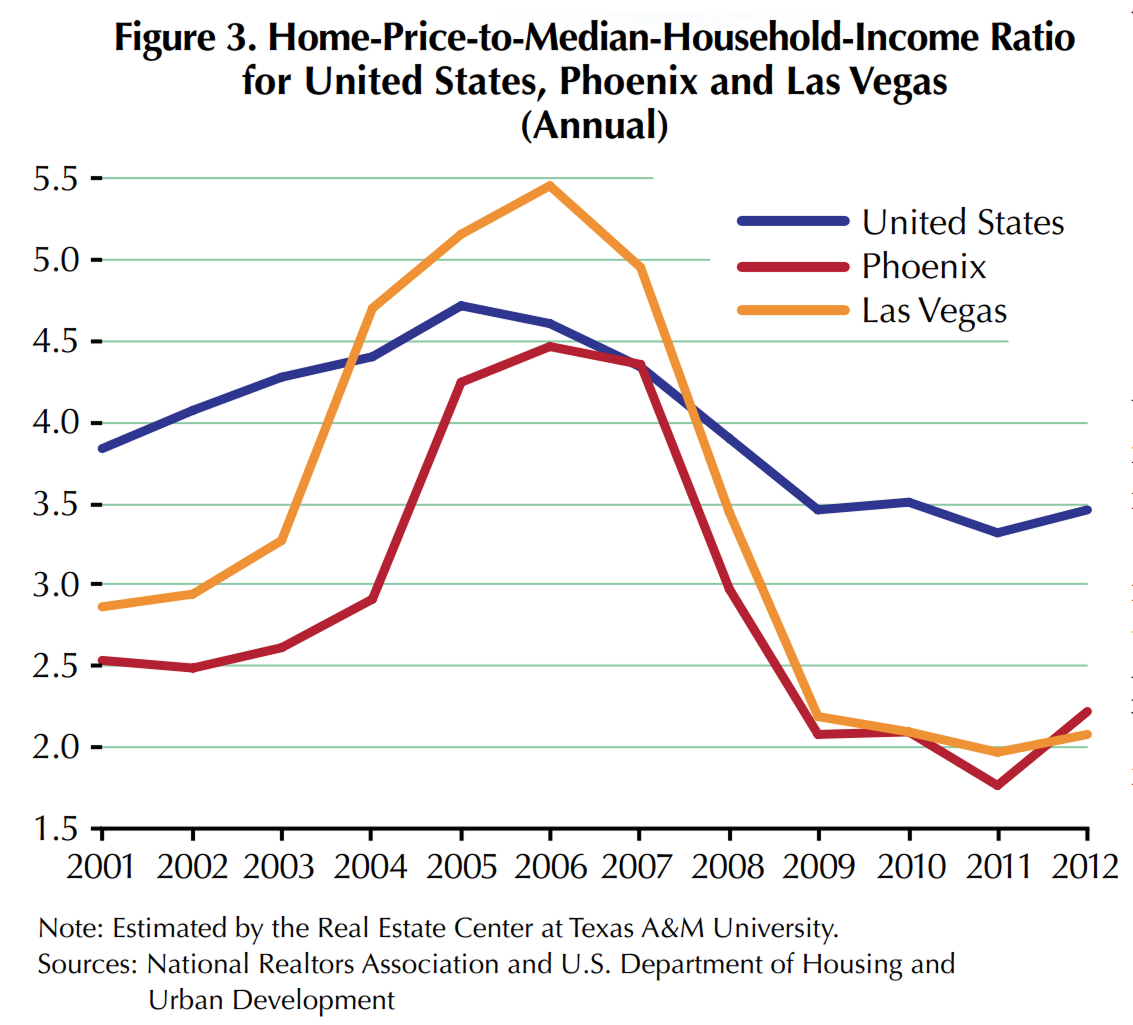

So, how did economic fundamentals behave? Can they explain the rapid price increases? Both Phoenix and Las Vegas registered faster growth in population, employment and income growth on average than the nation and the cities’ respective average historical trends (Tables 2, 3, 4). By contrast, the United States did not outperform its past 20-yearaverage historical trend in population and employment growth. Only GDP per capita registered a relatively higher average growth rate during that period. The ratio of home price to median income for both Phoenix and Las Vegas increased sharply during that period, as it did for the United States to a lesser degree (Figure 3).

This also held true for the ratio of home price to annual rents for both Phoenix and Las Vegas, which registered acute increases from 2002 to 2006. These data were a possible warning that price increases were not based on economic fundamentals related to median household income and annual rents, an important signal that a housing bubble had formed.

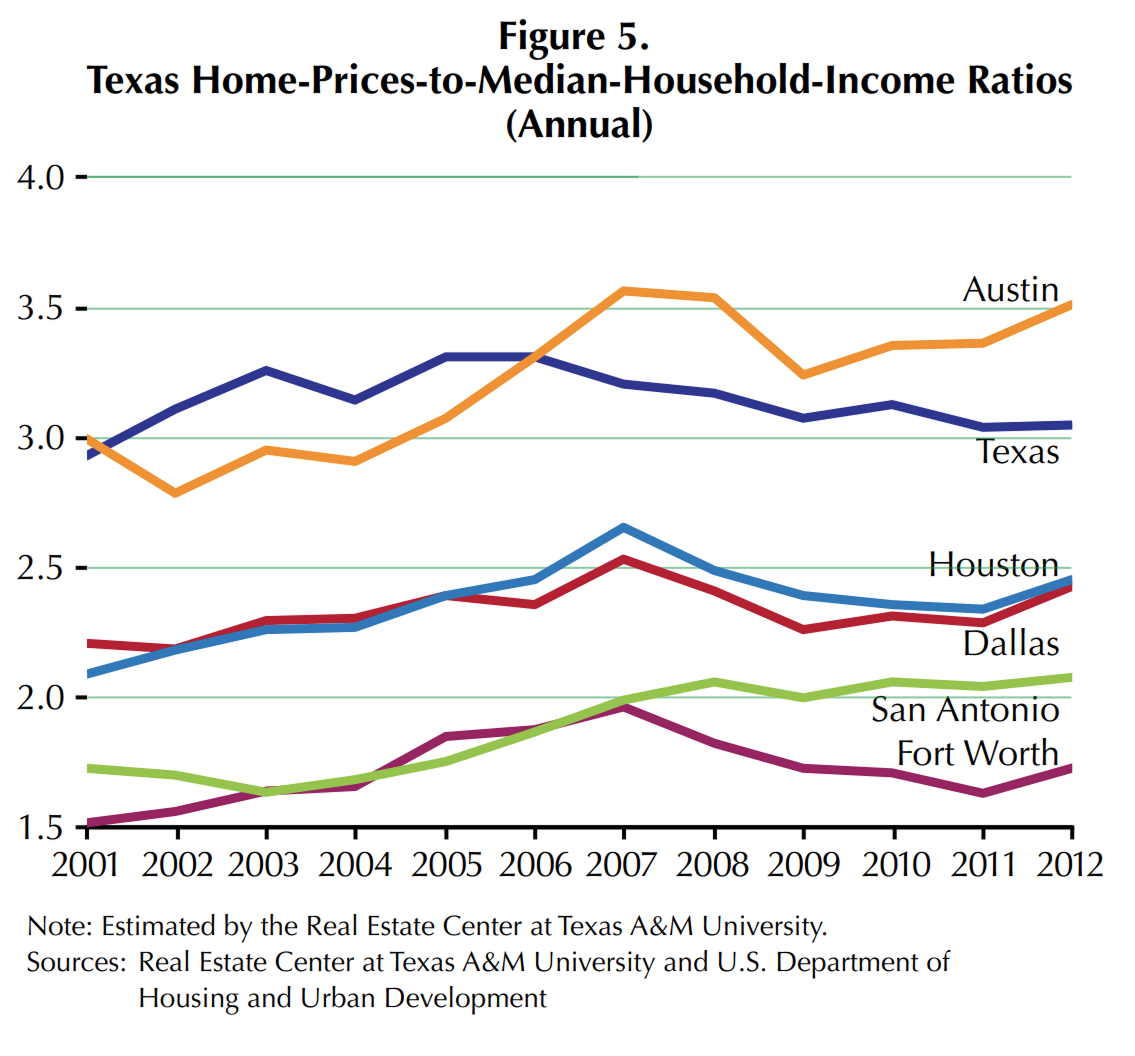

In contrast to Arizona and Nevada, the Texas housing market did not register such rapid home price increases during the housing boom cycle. Prices here were more in line with past price behavior for the region (Table 1). The relationship between home prices and economic fundamentals in Texas and its major MSAs shows that population and employment grew faster in Texas and the majority of its MSAs than in the United States but was below the state’s average historical trend (Tables 2, 3, 4). However, GDP per capita for Texas and its major MSAs grew at a lower average rate compared with the nation. Houston’s GDP per capita decreased. Austin’s GDP per capita grew faster during the period and was higher than its ten-year average from 2002 to 2012. Ratios between home prices and median income and annual rents recorded small increases between 2006 and 2007 and, although they are higher, they still correspond to the behavior observed in previous years (Figures 5, 6).

Unfortunately, asset price bubbles and crashes in stocks and housing are here to stay, as human nature plays an important role in the shaping of speculative bubbles. The events of the recent housing bust demonstrate the enormous economic and financial costs associated with asset price bubbles and crashes.

Supply and demand determinants change over time, so there is no safe way of knowing what asset prices should be. Still, when analyzing long-run trends in asset prices, especially the housing market, their relationship to economic fundamentals can offer insight into possible bubble formation. Currently, Texas home prices are based on strong fundamentals, but when expectations start to exceed real outcomes and current price increases are extrapolated into the future, beware. This assumption has been proven to be dangerously incorrect.

For more information, see Real Estate Center publication 2047, Housing Bubbles and Economic Fundamentals.

Dr. Torres ([email protected]) is an associate research economist with the Real Estate Center at Texas A&M University.

Did you like this Article?

You might also like

6 minute read

Jul 10 2013

Land, Lots of Land: How Texas Dodged the Housing Bubble

Forget all the references to a “home price” bubble in the mid-2000s. Center research reveals that it was a “land price” bubble that caused havoc in California, Nevada and other states. As for Texas, it flew above the crisis thanks to plentiful land and less restrictive development processes.