Capitalization rates can be a useful tool when making commercial investment decisions. A Real Estate Center study found that cap rates in Texas’ major metros have recently trended downward but are generally higher than other key rates.

Mar 16, 2020

A Calculated Risk

Commercial Real Estate Profitability

Commercial real estate investment carries some degree of risk, of course. Fortunately, there are tools that can, for example, provide clues as to which major Texas metro poses the least amount of risk overall.

All commercial real estate investments involve some risk because of the uncertainty of future revenue and expense streams. Since owners of capital can invest in alternative investment projects, several measures of profitability have been developed to help investors select projects that maximize profits. One is the capitalization, or cap, rate.

In general, the higher the cap rate, the higher the risk. Investors compare cap rates for potential projects with their cost of funds when selecting investment projects, considering only those investments where the cap rate exceeds the cost of funds. If funds are borrowed to finance the investment, the borrowing cost is equal to the interest rate charged on loans. In an all-equity investment, the cost of funds is the opportunity cost of using capital in alternative investments with similar risk.

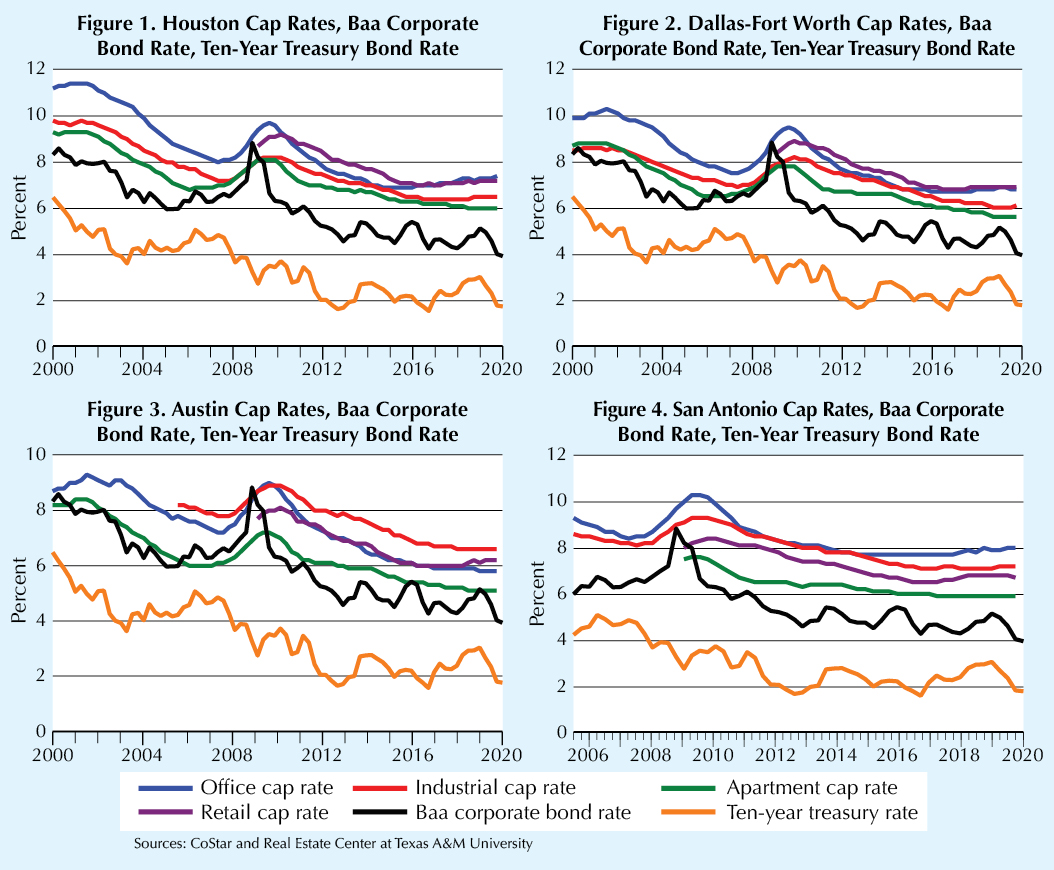

The Real Estate Center used a quarterly time series of cap rates to investigate the profitability of apartment, office, retail and industrial sectors in Texas’ four major Metropolitan Statistical Areas (MSAs) (Figures 1-4). Depending on data availability, the time period for each cap rate begins in first quarter 2001 or later and ends in third quarter 2019. The study used CoStar Group’s market cap rates. Moody’s Baa corporate bond rate and the ten-year Treasury rate are shown for comparison.

Except during the Great Recession (GR) of 2007-09, cap rates in the major metros were mostly higher than Baa corporate bond rates and well above ten-year Treasury rates.

Commercial cap rates in the four MSAs trended downward before the subprime mortgage crisis of 2007-10, when availability of low-cost mortgage funds led to increasing housing prices of all types, including apartments (Figures 1-4). Consequently, dividing net apartment rents by higher apartment prices resulted in declining cap rates. The downward trend reversed in the housing crisis of 2007-10 and the GR. During this period, the growth rate in most residential housing prices slowed dramatically, becoming negative in several regional markets.

In the bond markets, a flight to safety from 2007-10 led investors to sell corporate bonds and purchase U.S. Treasuries, pushing up corporate bond rates and pushing down Treasury rates. To help the U.S. economy recover from the GR, the Fed lowered the Fed funds rate, its monetary policy rate, to the lower zero bound to decrease short-term rates. The Fed then turned to quantitative easing by buying mortgage-backed securities and long-term Treasury bonds to lower long-term interest rates. As long-term interest rates trended downward, more real estate investment projects with smaller cap rates became profitable, pushing cap rates even lower.

Apartment cap rates have remained the lowest among all commercial sectors since the GR in all four MSAs. This suggests investors have been willing to accept lower profitability for less risk when investing in the apartment sector.

Cap rates in Houston’s and DFW’s industrial markets are the second-lowest after the apartment market (Figures 1-2). Lower industrial cap rates in the two largest metros indicate more perceived industrial market stability there than in Austin and San Antonio, where industrial cap rates are higher.

Austin Least Risky CRE Market Overall

Risk can be estimated by computing the “spread,” the difference between the cap rate and some risk-free rate. Because commercial real estate investments are expected to generate streams of income over a long period, investors commonly use the U.S. ten-year Treasury rate as a risk-free rate.

Spreads between cap rates and the ten-year Treasury rates are indicators of risk as well as the general profitability associated with commercial real estate investments. Spreads for all four MSAs trended downward before the GR due to growing property prices and lower perceived risks (Figures 5-7). Data for the retail sector were not available prior to 2009 (Figure 8). Spreads reversed direction and trended upward in the 2007-10 housing crisis, reaching their peaks in 2009, then trended downward in a more volatile manner through 2018.

Spread patterns indicate Austin, except for its industrial sector, is the least risky market for commercial real estate.

Risk trends closely follow the same pattern in all four MSAs, indicating some macro-level factor influences them equally. Although all spreads have recently begun to increase, it is too soon to tell if this is a reversal of the downward trend or just short-term volatility.

Lesson Learned

Cap rate compression since the GR may lead some to believe returns have compressed as well. However, the decrease in interest rates, which is reflected in a lower cost of capital, must also be considered. The net rate of return may be similar to returns in earlier periods when cap rates were much higher.

Tracking movement in Baa corporate bond rates has shown to be a much better indicator of cap rate changes than the ten-year Treasury rate. Real estate professionals may want to consider monitoring this rate for added insight into commercial real estate markets.

____________________

Dr. Anari ([email protected]) and Dr. Hunt ([email protected]) are research economists with the Real Estate Center at Texas A&M University.

Did you like this Article?