- Out-of-Houston migration spiked after the 2017 storm.

- Property damage pushes people out of homeownership.

- Destruction was unevenly distributed socioeconomically.

- Damage-induced movers tend to relocate to higher-income neighborhoods.

Mar 25, 2024

Lessons from Harvey

How Natural Disasters Affect Homebuying Decisions

Little is known about how natural disasters affect Texans’ housing choices, but Houstonians’ response to Hurricane Harvey provides clues.

Natural disasters have short-term and long-term impacts on local demographics and housing markets. There is an immediate impact on economic activity amid damage to physical capital and infrastructure. These disruptions spill into labor markets by affecting transportation networks and as individuals focus on recovery. In the long-run, natural disasters typically lead to net out-migration, decreased income, and lower real estate values.

While the regional impacts of disasters are well documented, much less is known about how Texans have responded in terms of their housing and neighborhood choices. Housing market outcomes following disasters reflect the choices of those directly impacted and others whose choices may reflect awareness of the disaster. Households and businesses may change their location and investment choices based on an area’s perceived disaster risks.

These choices drive housing activity during the recovery process, and understanding the circumstances in a post-disaster market can make real estate professionals better equipped to find housing for their clients after these events. Moreover, household responses to natural disasters have important implications for changes to the local tax base and neighborhood composition. All these factors interact with policy decisions surrounding land use and building regulation, insurance markets, and disaster relief.

It’s possible to glean some insights from Hurricane Harvey, which wreaked havoc on hundreds of thousands of people in the Houston area when it struck in August 2017.

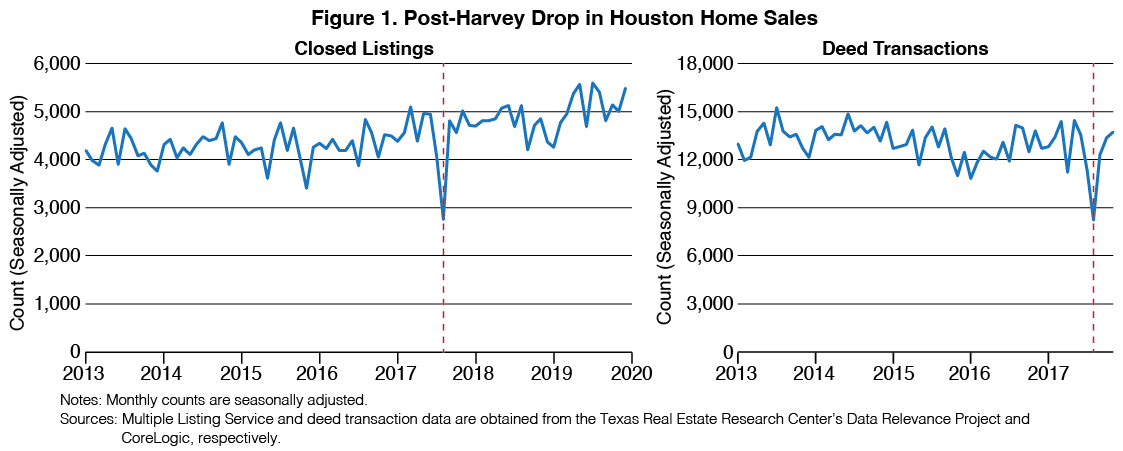

Harvey produced record-level rainfall that impacted more than 200,000 Houston homes, approximately 10 percent of the MSA’s housing stock, and caused $125 billion in direct damage. The shock to local home sales was immediate as the storm disrupted real estate transactions (Figure 1). Housing sales, however, normalized within a few months. A deeper understanding of disaster response is necessary to explain the recovery pattern.

Socioeconomics of Flooding

Flooding from Harvey was widespread, but the destruction was unevenly distributed. Those impacted were different socioeconomically for several reasons.

Individuals differ in their desire and ability to address disaster risk. Risk-averse individuals may select locations away from water sources or implement mitigation measures (e.g., the installation of flood vents). Others may value water as an amenity and prefer to live near the natural resource, increasing their risk of flooding. In some cases, they discount the risk relative to the benefits of being near the water.

Impacts also differ because communities may make different choices in terms of infrastructure investment and maintenance. This can lead to varying levels of local damage.

Historical development patterns also influence the differences in disaster impact. For instance, older neighborhoods may be near waterways because of the historic importance of water-borne trade.

Harvey’s Impact on Migration and Home Sales

It’s common for residents to leave an area in the wake of a natural disaster. Indeed, out-of-Houston migration spiked immediately after Harvey.

Migration rates were roughly the same in flooded and non-flooded census blocks, suggesting neighborhood-level damage played little role in individuals’ mobility decisions. Property-level damage, however, appears to have a bigger influence on behavior. Households exposed to $10,000 of flood damage were 40 percent more likely to move out of their pre-Harvey residence within six months of the storm compared with their non-flooded neighbors.

The initial wave of moves occurred in 4Q2017 and 1Q2018 before settling through 2019. Damage caused an immediate increase in within-county moves that persisted for nearly two years. In contrast, there was a delayed decrease in out-of-county moves that lasted several quarters before dissipating. Longer-distance moves may require more planning and may be more costly, potentially explaining the delayed response after a disaster.

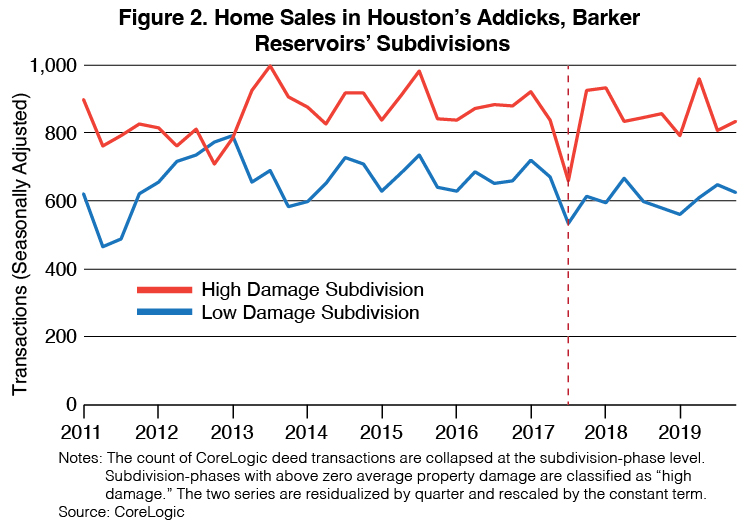

Economic theory predicts an aggregate decrease in home sales after natural disasters because of decreases in both housing stock and demand. Similar to the pattern in migration, there’s little relationship between neighborhood-level damage and home sales (Figure 2). The number of home sales in high- and low-damage subdivisions track similarly before and after Hurricane Harvey. If anything, high-damage subdivisions suffer a stronger shock on impact, then rebound higher for longer.

However, property-level damage caused home sales to drop in the short run. Suffering $10,000 of damage decreased the odds that homeowners would sell within six months by 21 percent compared with their non-flooded neighbors. The cumulative impact grew for about a year and persisted through 2019.

Homeowners considering moving may choose to repair their property before selling, and many flooded households were forced to wait months after Hurricane Harvey for full disbursement of disaster aid or insurance payments to help fund this investment.

Impact on Homeownership

While a natural disaster’s impact on relocation decisions lessens over time, the impact on homebuying is persistent.

For example, there is a substantial transition into renter occupancy for those who end up selling their house after suffering propety damage. Looking only at these movers, households exposed to $10,000 of damage are 3 percent less likely to own their next residence compared with their non-flooded neighbors. In other words, Harvey-related damage prevented roughly 1,100 home sales through 2019, resulting in around $300 million in lost dollar volume.

This change in housing consumption directly impacted household wealth. The transition from homeowner to renter occurred between 2017 and 2022, when Houston’s average sale price increased 42 percent. The average pre-storm home value for flood-exposed households who moved to rental properties was roughly $245,000. Applying the average increase in sale price, these homes would have surpassed an average of $347,000 by 2022. This appreciation, combined with an average of $73,000 of damage (a positive if the homeowner receives money from insurance or through government assistance) incurred by these households, suggests approximately $175,000 of potential lost wealth for households who became renters because of flooding.

Where do Impacted Homeowners Go?

Flood damage influences the types of neighborhoods and homes where individuals choose to live. Houston households impacted by flooding tended to move to higher-valued homes and higher-income neighborhoods. These changes in socioeconomic environment, combined with the estimated decrease in homeownership, highlight the potential tradeoffs in a post-disaster environment.

Since disaster damage pushes people out of their neighborhoods and into new economic environments, the impacts of extreme weather may extend into other aspects of life. These neighborhood effects may improve or hurt the transition into different types of housing.

The combination of results raises important questions about the effectiveness of disaster aid. For example, the delayed effect on housing transactions may indicate that Small Business Administration loans are keeping people from losing their homes immediately after catastrophic events. Despite this assistance, disaster damage eventually led to a substantial transition out of homeownership and into rental housing. It’s unclear what ought to happen because of this transition, especially as flooded households tend to relocate into higher income neighborhoods that may offer improved economic opportunities.

For more information, read Miller’s technical report How Natural Disasters Affect Homebuying Decisions.

_______________

Wesley Miller ([email protected]) is a senior research associate with the Texas Real Estate Research Center.

Did you like this Article?

You might also like

6 minute read

Mar 06 2018

Ebb and Flow

A Geographical Look at Houston's Stormy History

Recent history suggests that flooding is the new norm in Houston, a city with an extensive network of bayous, lakes, and other waterways. Research provides clues to what will happen—and in which neighborhoods—the next time a catastrophic storm strikes.

7 minute read

Sep 06 2018

Highs & Lows of Floodplain Regulations

Houston has adopted new building regulations intended to protect homes in the city’s most flood-prone areas. The regulations will increase new-home construction costs, but they could also have human and economic benefits. Whether those benefits will outweigh the cost increases is the big unknown.

5 minute read

Mar 06 2018

Imperfect Storm

Harris County averaged 40 inches of rain from Hurricane Harvey, nearly a year’s worth of rainfall. But if you think the storm’s deluge and ensuing floods hurt all Houston neighborhoods equally, think again. A recent Center study finds that lower-income neighborhoods were hit the hardest.