As the state’s population grows, so does the need for more housing. Here are the data and tools you need to keep up with housing market trends in your area.

Whether you’re talking about DFW’s financial services industry, Austin’s tech sector, Houston’s energy corridor, or the medical hub that is San Antonio, commercial real estate is big business in Texas.

Mineral rights. Water issues. Wildlife management and conservation. Eminent domain. The number of factors driving Texas land markets is as big as the state itself. Here’s information that can help.

Center research is fueled by accurate, high-quality, up-to-date data acquired from such sources as Texas MLSs, the U.S. Bureau of Labor Statistics, and the U.S. Census Bureau. Data and reports included here are free.

Stay current on the latest happenings around the Center and the state with our news releases, NewsTalk Texas online searchable news database, and more.

Established in 1971, the Texas Real Estate Research Center is the nation’s largest publicly funded organization devoted to real estate research. Learn more about our history here and meet our team.

Over the years, Texas wildfires have resulted in loss of life, loss of thousands of homes, and billions of dollar in direct economic impact. What can be done to mitigate their impact?

Over the past decade, wildfire losses in the United States have reached unprecedented levels. Nine of the ten costliest American wildfires have occurred since 2017, and the annual economic cost of wildfire in North America continues to rise. More than 238,000 wildfires have burned 12.6 million acres in Texas since 2005. The recent Smokehouse Creek Fire burned more than one million acres in February and March, making it the largest wildfire in Texas history and topping the state’s list in terms of agricultural losses. The East Amarillo Complex Fire of 2006 caused the largest loss of life with 13 fatalities, and the Bastrop County Complex Fire ranks as the state’s most destructive, with 1,673 homes lost in 2011.

Texas has two primary wildfire seasons, each of which are characterized by distinct determinants and risks. The winter (or early spring) wildfire season is concentrated in the western half of the state and depends on precipitation during the preceding summer to facilitate growth of vegetative fuel. Winter weather tends to kill this vegetation (or induce dormancy), creating conditions ideal for ignition and burning. Seasonal winds contribute to potential ignition events and rapid spread during the winter and early spring. In contrast, Texas’ summer wildfire season impacts the entire state and largely depends on intense heat that sufficiently dries out vegetation between rainfall events. Hotter temperatures are projected to amplify wildfire risk across Texas, particularly in the western portion of the state. Rising precipitation levels in more eastern regions serve to offset the impact of hotter temperatures on wildfire risk, but warmer winters may shift the current geography of wildfire seasons.

In addition to the impacts of climate change, population and land-use patterns directly affect the likelihood of wildfires and the magnitude of destruction. Between 2005 and 2021, 85 percent of Texas wildfires were ignited within two miles of a community. This two-mile distance often describes the wildland-urban interface (WUI) zone (i.e., the area of transition between unoccupied land and human development). While the WUI is a major source of ignition, it also carries complex challenges in terms of wildfire suppression. For example, wildland firefighting techniques and equipment emphasize the protection of natural resources, while structural firefighting focuses on saving human life and the built environment. The transitional nature of the WUI presents additional complexities in terms of political, economic, and social dimensions, all of which affect investment in resilient infrastructure as well as potential disaster recovery.

IN FALL 2011, Bastrop (pictured here) was the site of the most destructive wildfire in the state’s history. The Austin American Statesman reported that the wildfire “burned 34,356 acres, scorching countless neighborhoods, dozens of commercial structures, and around 1.5 million trees.”

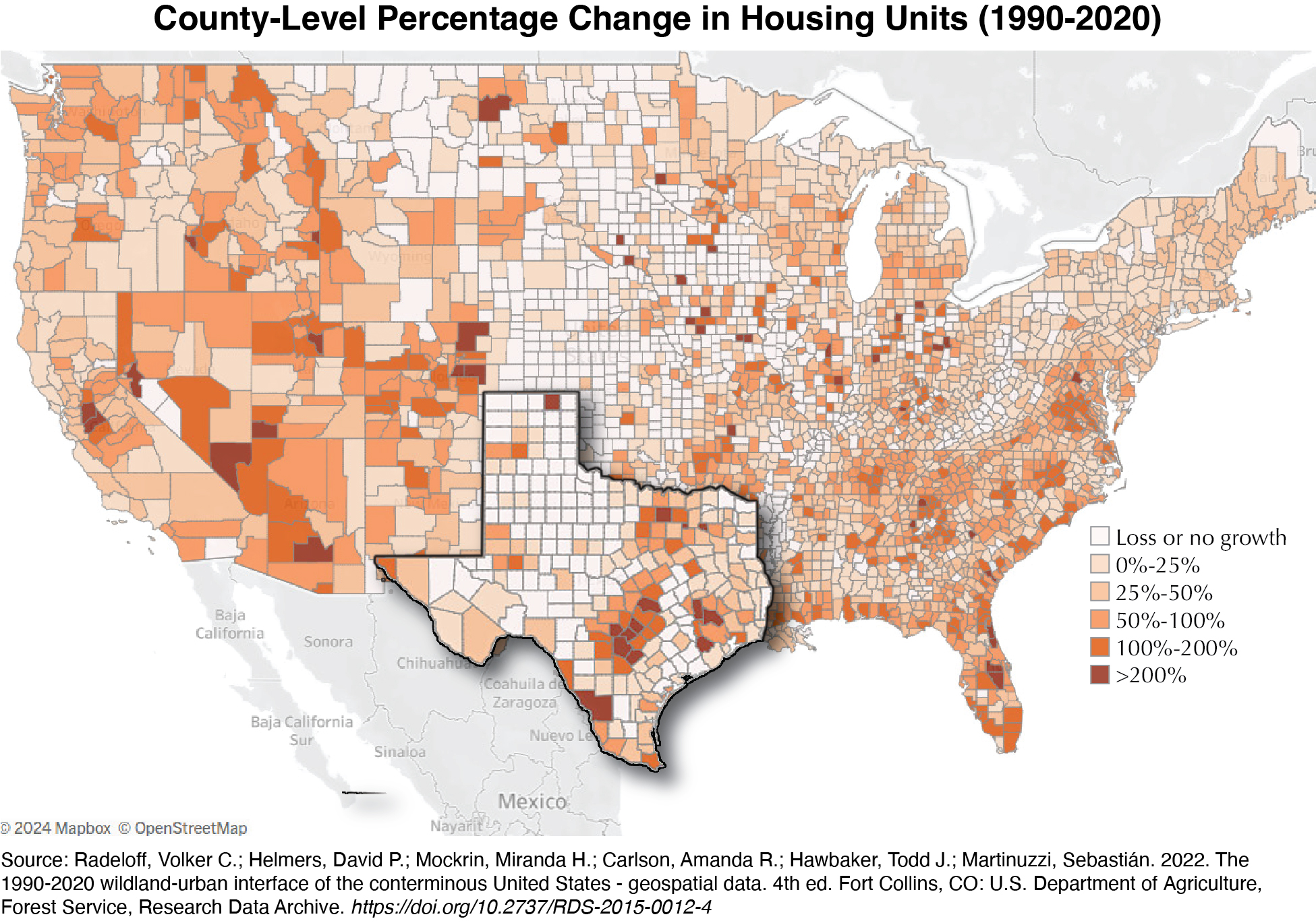

Explosive Growth in the WUI

The Texas WUI stretches across 11 million acres and contains 3.2 million housing units (ranking second nationally behind California). More than 25 percent of Texas homes lie in the WUI, underscoring the significant intersection of residential development and the natural environment.

While total land mass correlates with absolute rankings, the number of housing units in Texas’ WUI increased 82 percent from 1990 to 2020, outpacing 42 of the 48 contiguous states. Rapid development in the WUI exceeded statewide growth in housing units by 13 percentage points during the same period. While WUI growth has occurred across large swaths of the state, the map illustrates hot spots of expansion northeast of Houston, outside Dallas and Fort Worth, between Austin and San Antonio, and along the Texas-Mexico border.

Disproportionate growth in the WUI aligns with several socioeconomic developments. Texas’ economic vibrance is attracting domestic and international migrants while retaining a substantial share of the Texas-born population. These population patterns translate into increased demand for housing, particularly within driving distance of major metropolitan areas. The scarcity of urban land combined with regulatory barriers to dense development (e.g., minimum lot sizes) inhibits the housing-supply response, creating local shortages that push prices upward and populations outward. The suburban landscape is often associated with infrastructure investment, lower crime rates, and larger homes that may be disproportionately preferred by certain subpopulations (e.g., households with children). Demand for these amenities contributes to development in the WUI, and the post-COVID-19 economy characterized by remote work and preferences for more physical space portend persistent demand for the foreseeable future.

Wildfire Adaptation Strategies

The combination of climate change and Texas’ growth patterns increases the state’s exposure to wildfire risk. Understanding the development and reconstruction of the WUI after wildfires is essential to quantify future risk and inform adaptation decisions. Wildfire adaptation depends on four primary pillars: self-protection, self-insurance, public investment, and market insurance. These four channels interact together in complementary and/or counteracting ways.

Self-protection pertains to individuals reducing their probability of exposure, typically by relocating to less risky areas. Relocation decisions, however, depend on a variety of factors, including proximity to family, changes in household composition, labor market considerations, and financial standing. The cost of moving (and other transaction costs) inhibits relocation, particularly for lower-income households, even in the context of heightened risk. High levels of personal attachment to a location may also limit large-scale relocation. Moreover, self-protective measures are available only to individuals, not to physical communities.

Self-insurance refers to individual actions that reduce the magnitude of potential losses. These actions include the adoption of nonflammable or fireproof construction materials and property-level vegetation management. Increased demand for these solutions will incentivize the innovation of new products, introducing new adaptation options. Individuals who invest in property-level improvements could become more attached to their property and reduce their likelihood of moving. As with the self-protection channel, the cost of self-insurance affects adaptation inequities. The cost of adaptive technology, however, may decrease over time due to subsequent innovation, economies of scale, or public subsidies. Individuals’ self-insurance actions may have benefits that spill over to neighboring properties (e.g., less fuel on one property reduces the probability of ignition or spread to nearby properties), suggesting a potential role for public subsidies to offset underinvestment.

Another adaptation channel is to rely on public investment in spatial protection such as fire management practices (e.g., controlled burns and allowance of “natural” fires) and fire suppression resources. Community-level improvements in wildfire resilience and quality of life directly impact property owners through higher land prices and rents, incentivizing a collective interest in advocating for public investment. While fire protection in urban areas is directly provided by local governments, fire management around the WUI often falls under state or federal responsibility.

Federal and state fire protection services incentivize growth in these higher-risk areas by lowering local infrastructure and maintenance costs, effectively forcing state and national taxpayers to subsidize investment in the WUI. The presence of state or federal resources serves as a place-based subsidy that encourages people to take risks they would have otherwise avoided (known as a moral hazard effect).

For example, the spatial arrangement of houses and vegetation within the WUI impacts the extent of structural damage from wildfire, but homeowners do not fully take the expected costs of future fire protection into consideration when making residential decisions. Similarly, local communities do not fully incorporate these same costs in their land-use and building-code policies. Post-fire adaptation typically focuses on building standards and lot-scale vegetation management. Such policies that encourage self-investment, self-protection, or the internalization of public investment costs may mitigate moral hazard.

Market insurance is the fourth pillar of wildfire adaptations. The inevitability of risk makes the insurance system a necessary component for climate resilience, enabling wildfire victims to recover after destruction. Most standard homeowners insurance policies cover wildfire damage, and these policies are governed at the state level. Like most states, Texas requires insurance companies to file rate changes for review to ensure that rates:

are adequate;

are not excessive (i.e., do not produce an unreasonably high long-term profit compared to the coverage provided);

are based on sound actuarial principles;

are reasonably related to all costs (expected losses and expenses); and

are not based on the insured’s race, creed, color, ethnicity, or national origin.

The Texas Department of Insurance approved 91 percent of rate filings in 2023, resulting in an average effective rate increase of 23 percent for owner-occupied homeowners’ filings. While higher insurance rates are often lamented, they play an important role in communicating risk. Rising rates have distributional consequences and highlight the unequal exposure to environmental risk. In efforts to relieve pains caused by these price pressures, some states have implemented additional insurance-rate regulations, such as prohibiting increases above a fixed percentage). An unintended consequence of these efforts is a distortion in the price signal that makes at-risk land cheaper, thereby incentivizing excessive exposure to wildfires.

Rebuilding in the WUI after Wildfires

Some wildfire risk is inevitable, and understanding the response to disasters provides an important framework for the future. Wildfire destruction is often discussed in the context of residential real estate. While destroyed buildings decrease housing supply, the net effect on the supply of developable land is ambiguous. Heat from fires can damage foundations and surrounding infrastructure, serving to impede redevelopment (thereby decreasing the supply of developable land, at least in the short run). Not all damaged property, however, suffers this fate during wildfires, potentially muting the land-supply shock. If the supply of land exists and the demand for housing persists, then redevelopment would be expected to occur in the WUI.

In addition to the magnitude of reconstruction, several factors affect the pattern of redevelopment. First, the location of surviving infrastructure (e.g., roads and utility lines) offers incentives to rebuild using existing spatial arrangements. It may be cost-effective to reuse rather than to start anew.

Second, the complexities surrounding disaster aid and recovery may push efforts toward the pre-wildfire status quo. The WUI spans multiple municipal, state, and national jurisdictions, creating a patchwork of processes for community development, infrastructure management, and future disaster preparation.

Third, the demand for many amenities in the WUI corresponds directly to wildfire risk. For example, households may demand the “Arcadian” intermixing of houses and vegetation on large lots that typically characterizes development in the WUI, and this spatial arrangement is particularly susceptible to wildfire ignition and spread. The utility derived from these characteristics may outweigh their associated risks (at least from the household perspective), similar to a scenario of strong demand to live on a coastline faced with sea-level rise. The combination of these forces not only affects the magnitude and geography of development in the WUI but also its social and economic arrangements moving forward.

____________________

Wesley Miller is a former senior research associate with the Texas Real Estate Research Center, and N. Lee May is a doctoral candidate with Texas A&M University’s Department of Ecology and Conservation Biology.

Download PDF

Did you like this Article?

In This Article

Contents

Key Takeaways

Eighty-five percent of Texas fires ignite within two miles of a community, and economic exposure is projected to increase due to climate change and population growth patterns.

There are several ways the population can adapt to higher wildfire risk, including self-protection activities and insurance. Some policies may encourage additional building development in risky areas.

The potential to rebuild depends on factors such as underlying demand and the condition of local infrastructure.

You might also like

Single-family

10 minute read

Mar 25 2024

How Natural Disasters Affect Homebuying Decisions

The combination of climate change and economic growth in disaster-prone regions increasingly exposes Texas’ population to extreme weather events (IPCC, 2023). Natural disasters have an immediate impact on economic activity and typically lead to net out-migration, decreased income, and lower real estate values (Boustan et al., 2020).

Understanding Homeowner Insurance Forms and Coverage Limits

Breaking news: Insurance is complicated. This guide to the different types of perils, policy forms, and coverage types can help you better understand your choices for property coverage and make informed decisions.

The winter wildfires in Texas have prompted media and community concerns. Will these fires, which include the so-called Smokehouse Creek Fire (now the largest wildfire in the state's history), become a homeowners insurance...

As the state’s population grows, so does the need for more housing. Here are the data and tools you need to keep up with housing market trends in your area.

Whether you’re talking about DFW’s financial services industry, Austin’s tech sector, Houston’s energy corridor, or the medical hub that is San Antonio, commercial real estate is big business in Texas.

Mineral rights. Water issues. Wildlife management and conservation. Eminent domain. The number of factors driving Texas land markets is as big as the state itself. Here’s information that can help.

Center research is fueled by accurate, high-quality, up-to-date data acquired from such sources as Texas MLSs, the U.S. Bureau of Labor Statistics, and the U.S. Census Bureau. Data and reports included here are free.

Stay current on the latest happenings around the Center and the state with our news releases, NewsTalk Texas online searchable news database, and more.

Established in 1971, the Texas Real Estate Research Center is the nation’s largest publicly funded organization devoted to real estate research. Learn more about our history here and meet our team.