Quantifying Higher Mortgage Rates’ Effect on Housing Affordability

In his latest blog post, TRERC’s Josh Roberson talks about how mortgage rate changes have impacted housing affordability over the past five years.

Over the past few years, historically low mortgage rates have played a major role in boosting both home sales and refinance activity in Texas. In a short time, however, those rates climbed quickly and took a big bite out of housing affordability.

Data collected by the Consumer Finance Protection Bureau quantify some of the changes in affordability that hit homebuyers between 2019 and 2023.

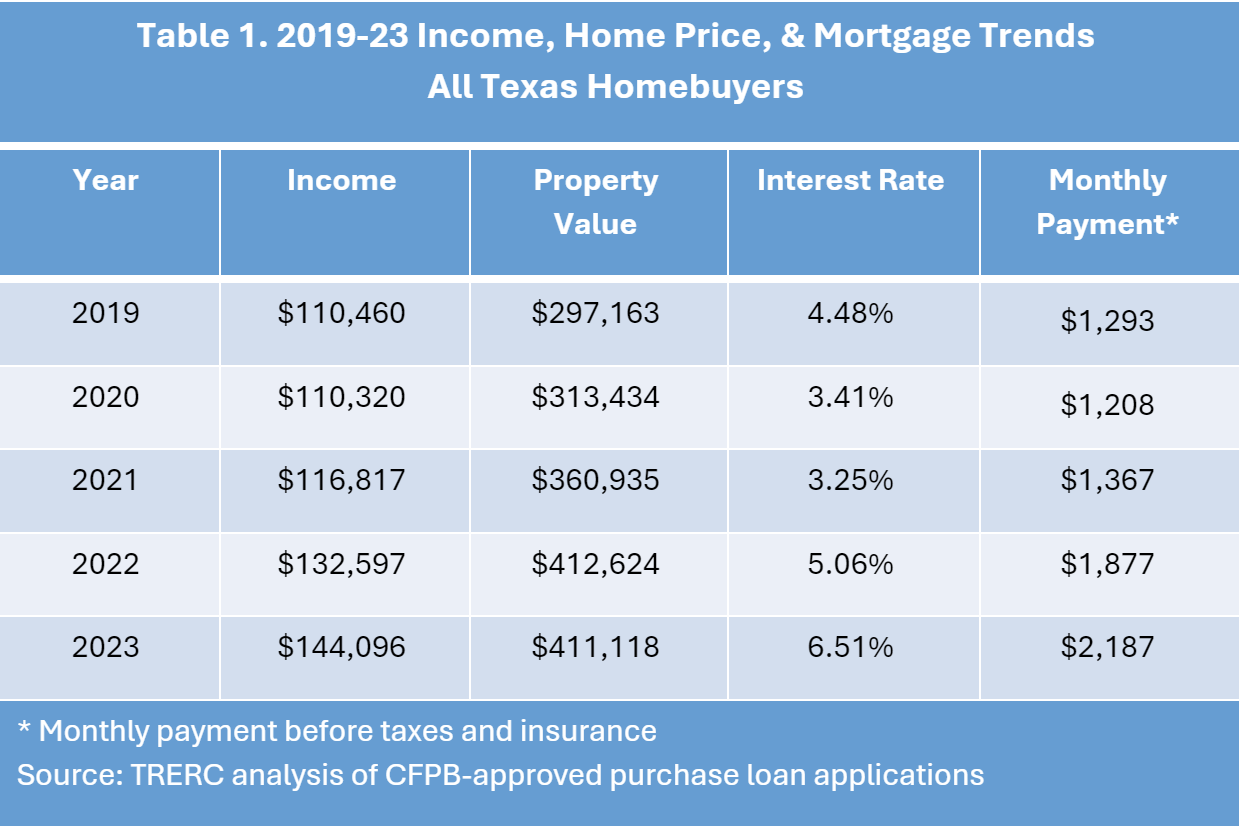

Beginning in 2019, the year before COVID and the massive drop in interest rates, the average mortgage rate was 4.48 percent, and the average home value was $297,163 (Table 1). Estimated loan payments before property taxes or homeowners’ insurance were $1,293 per month.

Home prices increased dramatically over the next two years, reaching an average of $360,935 in 2021. More importantly, interest rates fell to their lowest point—an average of 3.25 percent. Despite over a $60,000 increase in average home value, the big drop in interest rates resulted in only a $74 increase in monthly loan payments. Fast forward another two years when home values increased an additional $50,000, reaching $411,118. Mortgage rates, on the other hand, doubled to 6.51 percent, resulting in a new average loan payment of $2,187.

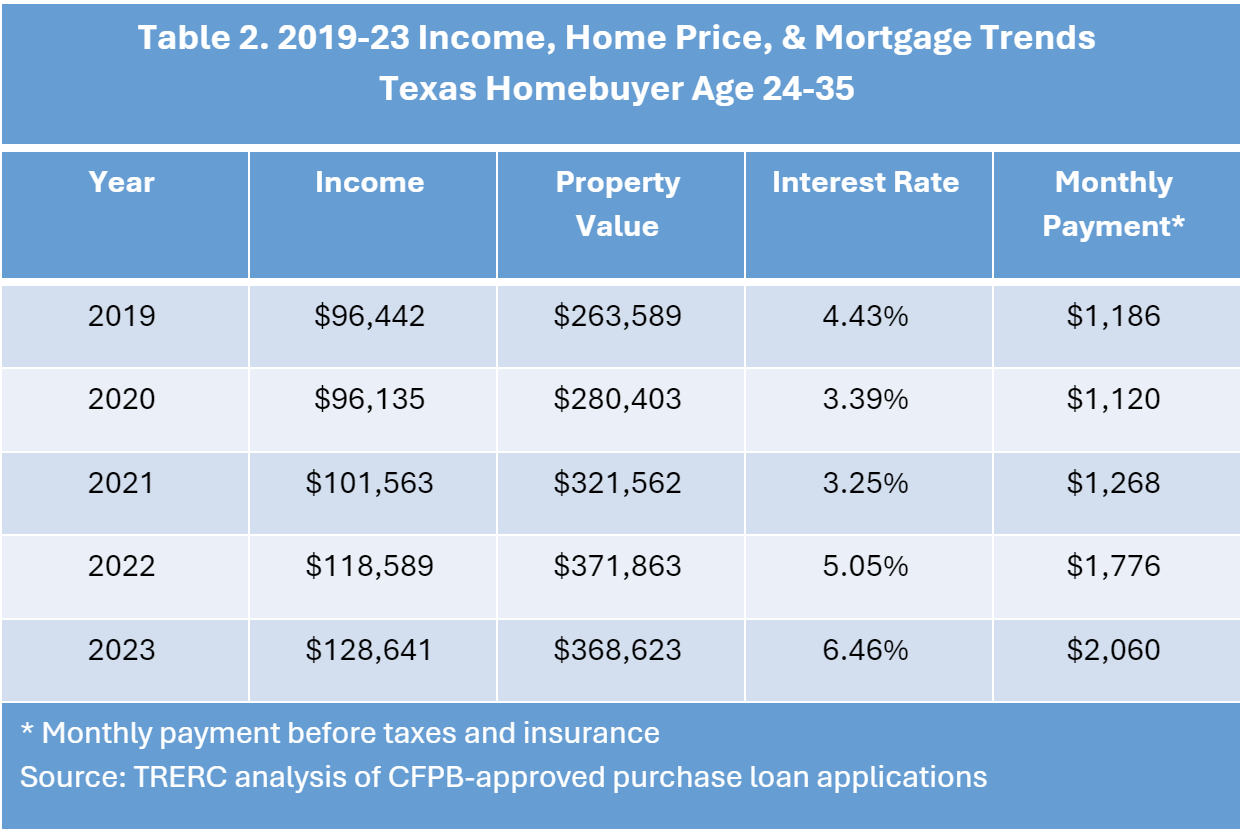

The biggest age cohort for homebuyers during this time was 25- to 34-year-olds. Not only is this cohort the largest, it’s also significant for affordability since many of these applicants are first-time buyers. Over the same five-year window, the average price of homes purchased by this cohort jumped from $263,589 to $368,628 (Table 2). Based on a comparable swing in rates, mortgage payments increased 74 percent from $1,268 to $2,060.

Looking forward, price growth has slowed but actual home values have been fairly resistance to downward pressure. After peaking in mid-2022 at $360,000, median statewide home prices have hovered between $330,000 and $340,000 for two years with no signs of changing anytime soon. Mortgage rates have fallen but are not expected to return to anywhere near the low points of 2020 and 2021.

While mortgage rates and home prices drastically influenced affordability, other factors have also added pressure. Property taxes and homeowners’ insurance have grown considerably over the same period. Additionally, household incomes have grown, but not at the same rate as home prices. Ultimately, homebuyers are under a lot more financial pressure to afford housing costs.

I’ll look at the refinance side and its potential impact on housing supply in a future post.

Views expressed on The 338 are those of the authors and do not imply endorsement by the Texas Real Estate Research Center, Division of Research, or Texas A&M University.

You might also like

Texas Housing Insight | October 2024

Home sales typically cool off by October, but this year is a little different with sales in both September and October higher than they were during the summer. The rate of new listings is still on the rise resulting in rising inventory levels.

Housing Affordability In Limbo

Texas housing affordability has improved as both average home prices and average mortgage rates decreased. In the third quarter of this year, the Texas Home Affordability Index (THAI) increased to 1.11 from 1.04 the quarter before (Figure 1). This time last year, the index was at 1.03.

What is the Impact of Rate-Locked Buyers on Residential Sales?

Rate lock-in describes a scenario where leveraged homeowners are disincentivized to purchase another home because prevailing interest rates sufficiently exceed the fixed rate guaranteed on their existing mortgage.

Tierra Grande

Check out the latest issue of our flagship publication.