- Proximity to water or high-risk areas affects premiums and coverage availability.

- Housing material and style impact wind damage susceptibility, influencing insurance costs.

- Newer homes may have lower premiums due to better construction.

Jul 15, 2024

What Drives Wind and Flood Insurance?

Summer means vacations, afternoons at the pool, and nights at the ballpark. It also means the beginning of hurricane season, making this an appropriate time for a discussion of factors that impact wind and flood insurance.

Homeowners in most parts of the state occasionally have to contend with windstorms, whether hurricanes or tornadoes, and those in or near coastal regions often have the added risk of flooding. For many of these homeowners, windstorm and flood insurance are necessary considerations. In some areas, such insurance is required.

Nearly 20 factors determine a homeowner’s insurance premium, deductible, and coverage limits, but four factors have a greater impact when homes are subject to the perils of windstorms and flooding. Homeowners need to understand each of these.

Location is Key

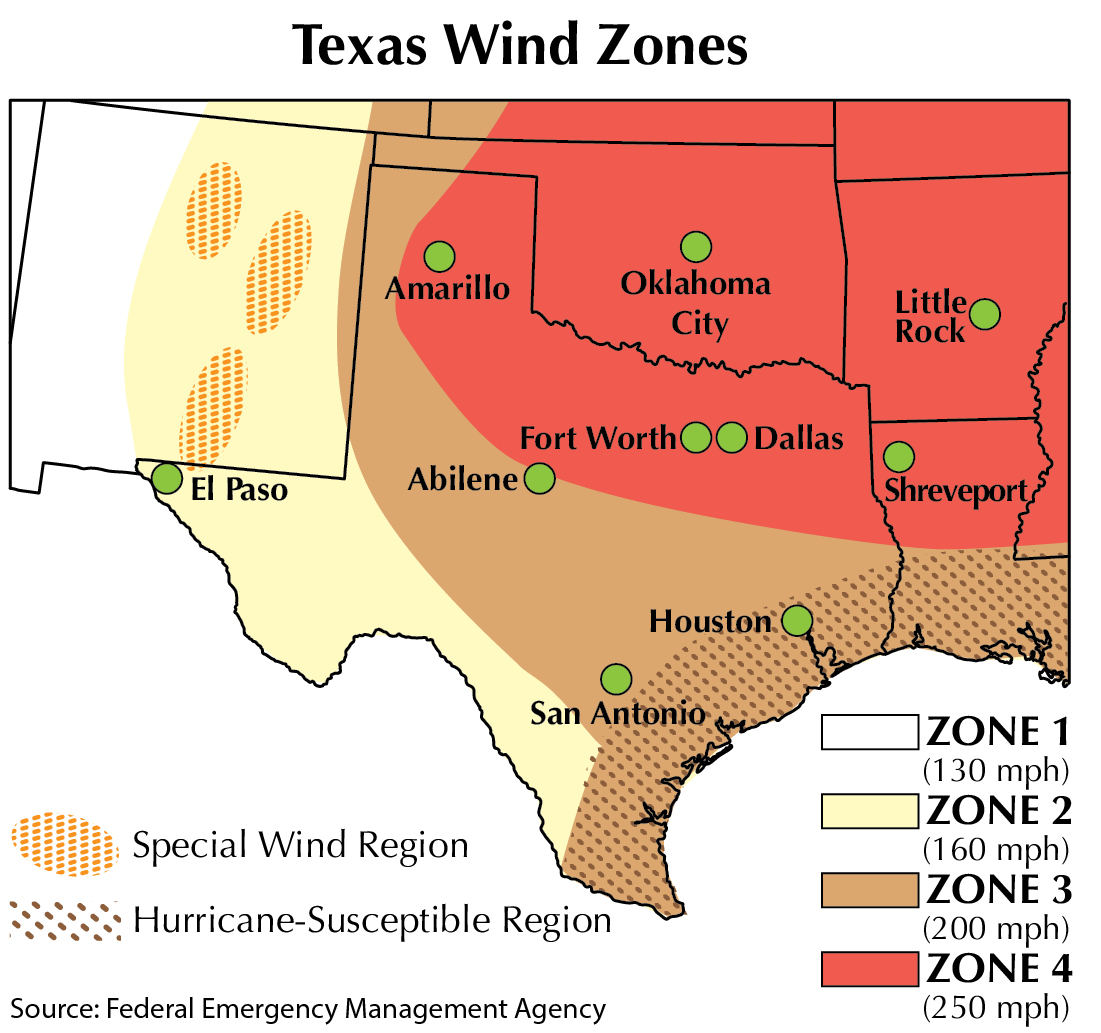

The home’s location is probably the most critical factor. Homes located near coastal areas are subject to hurricanes, tornadoes, and flooding, whether wind-driven or the result of tidal surge or overflow. Homes located away from the coast—such as in the Panhandle, West Texas, and the Hill Country—are still subject to tornadic and straight-line winds. Wind speed maps for the United States, which show how the strength of extreme windstorms varies across the country, typically show four wind zones, each differentiated by predicted wind speed:

- Zone I: winds up to 130 mph.

- Zone II: up to 160 mph.

- Zone III: up to 200 mph.

- Zone IV: up to and beyond 250 mph.

While these maps were created to help design storm shelters and safe rooms in the affected areas, they can also be used to extrapolate the severity of wind speed and how those speeds would affect structures not designed to withstand such forces. Data on wind speed and wind direction, along with other meteorological measurements, are loaded into computer models to forecast winds. When combined with historical data from past events, the resulting map depicts the frequency and strength of windstorms.

This type of map is used primarily to develop national and international building codes intended to protect human life, but the codes can also have the ancillary benefit of minimizing property damage.

Three of the four wind zones are present in Texas (see map). Zone IV covers the area north of a line drawn from Beaumont to Abilene to Amarillo. Zone III lies south and west of Zone IV, stretching south past San Antonio to the southeast corner of New Mexico and the far western edge of the Panhandle. Zone III is further subdivided into a hurricane-susceptible corridor covering the area west of Houston and south to Mexico. Zone II is south and west of Zone III, stretching from San Antonio to the southeast corner of New Mexico. Zone I is not present in Texas.

Flood zones are determined in a similar manner, but there are 15 separate major designations. These are grouped by letter designation into ten high-risk zones (A and V), four moderate-to-low risk zones (B, C, and X), and one “indeterminate risk” zone (D). These zones are further broken down according to the type of flooding, depth of flooding, and likelihood of flooding. These zones are shown on a Flood Insurance Risk Map, or FIRM.

Properties financed with federal funds (such as through the VA or FHA) and located in one of the FIRM’s ten high-risk zones must be insured under the National Flood Insurance Program (NFIP). These properties are in a 100-year floodplain and have a 26 percent chance of flooding during a 30-year mortgage term. Owners of properties in the moderate-risk flood zones, the 500-year floodplain, or in low-risk flood zones (areas beyond the boundaries of the 500-year floodplain) can voluntarily participate in the NFIP or attempt to purchase flood insurance from their homeowners’ insurance company. NFIP premiums are high and the limits low, but these costs could be much lower than the cost of no coverage. In addition, the NFIP has a 30-day waiting period for insureds who voluntarily participate before flood insurance becomes effective.

In general, most insurance companies will readily offer some amount of flood coverage as an endorsement to the homeowner’s policy for low-risk areas. In moderate- or high-risk areas, flood coverage may be challenging, expensive, or impossible to obtain.

One important note: although the insurance industry uses the information about wind zone territories and flood zone designations, it does not determine those territories and designations. Those were created by the Federal Emergency Management Agency (FEMA), other governmental agencies, and universities.

Design and Build

When determining rates and coverage limits, insurers factor in a home’s building materials (frame, brick veneer, masonry, etc.), style (for example, multilevel versus ranch), and overall construction.

First, homeowners should understand wind load, which is a measure of the dynamic pressure wind puts on a surface. Dwellings are subjected to three types of wind force:

- uplift pressure that can cause a roof to rip away;

- shear pressure, a horizontal pressure that causes tilting or leaning; and

- lateral pressure that causes movement or sliding.

Homes designed with large, flat surface areas collect more wind load than homes with smaller surface areas. Similarly, designs that force wind into a small area increase the wind load on the structure. Openings such as doors and windows are structurally weaker than adjoining walls, and their failure allows more wind load to build inside the structure. For home construction tips, see sidebar.

When it comes to flood insurance, the foundation, openings, the structure’s height above the NFIP base flood elevation, fill, and erosion control become relevant factors in the insurer’s decision-making process. Most floods are not raging torrents of debris-filled water, but rather gradual inundation without significant currents. In areas where flooding is accompanied by more forceful movement of water, wall construction becomes an additional factor.

Raising the Roof

Both the type of roof and the roofing materials factor into the extent of damage from windstorms (but are obviously not a significant factor when it comes to flood damage). A hip roof, with the roof sections meeting at a point, creates an aerodynamic shape that allows wind to flow over the surface more readily, while a gable roof provides two flat vertical surfaces at the ends that are easily subjected to wind load (see figure). Hip roofs are effective against wind, but they are costly to build and repair.

Eaves can present additional problems. A roof with a large eave overhanging the wall can readily redirect horizontal wind, turning it into an uplift force. Eaves should not extend far from the wall to minimize uplift pressure, and all roofs should be strapped and anchored firmly to the foundation.

This Old House

The last major factor is age. Simply put, a newer home is more likely to be in better repair than an older home, resulting in less damage from wind.

More important, though, are the recent improvements in wind-specific and flood-specific building codes based on research various organizations—primarily the American Society of Civil Engineers (ASCE)—and universities in areas affected by severe windstorms have conducted in conjunction with FEMA. These collaborations have resulted in many ASCE standards that govern construction techniques to prevent or reduce wind- and water-related losses to structures.

Choosing to build or purchase a home is a major financial commitment—a balance of costs and benefits. But when the home is exposed to windstorm and flood, the cost/benefit equation and the balance of aesthetics and safety must be reconsidered.

____________________

Richard Rudolph, Ph.D. ([email protected]) is a research fellow with the Texas Real Estate Research Center and has 20 years of experience in insurance brokerage and 30 years of experience in insurance and risk management consulting and education.

Did you like this Article?

You might also like

Single-family

7 minute read

Feb 07 2023

What Does Homeowners Insurance Really Cover?

Not all homeowners insurance policies are created equal, and they may not always cover what you think they do. Read this quick overview to learn more (and have a copy of your own insurance policy handy when you do).

Single-family

8 minute read

Jan 29 2024

String of Perils

Understanding Homeowner Insurance Forms and Coverage Limits

Breaking news: Insurance is complicated. This guide to the different types of perils, policy forms, and coverage types can help you better understand your choices for property coverage and make informed decisions.