Commercial Roundup

Texas’ office markets are undergoing a dramatic reshuffle as post-COVID workplace policies reshape tenant demand. How are local job trends, new construction, and shifting preferences transforming markets in the state’s major metros, and what could it mean for the future of office real estate?

This inaugural installment of our quarterly commercial column highlights the shifting fortunes of Texas office buildings with a focus on trends by property class.

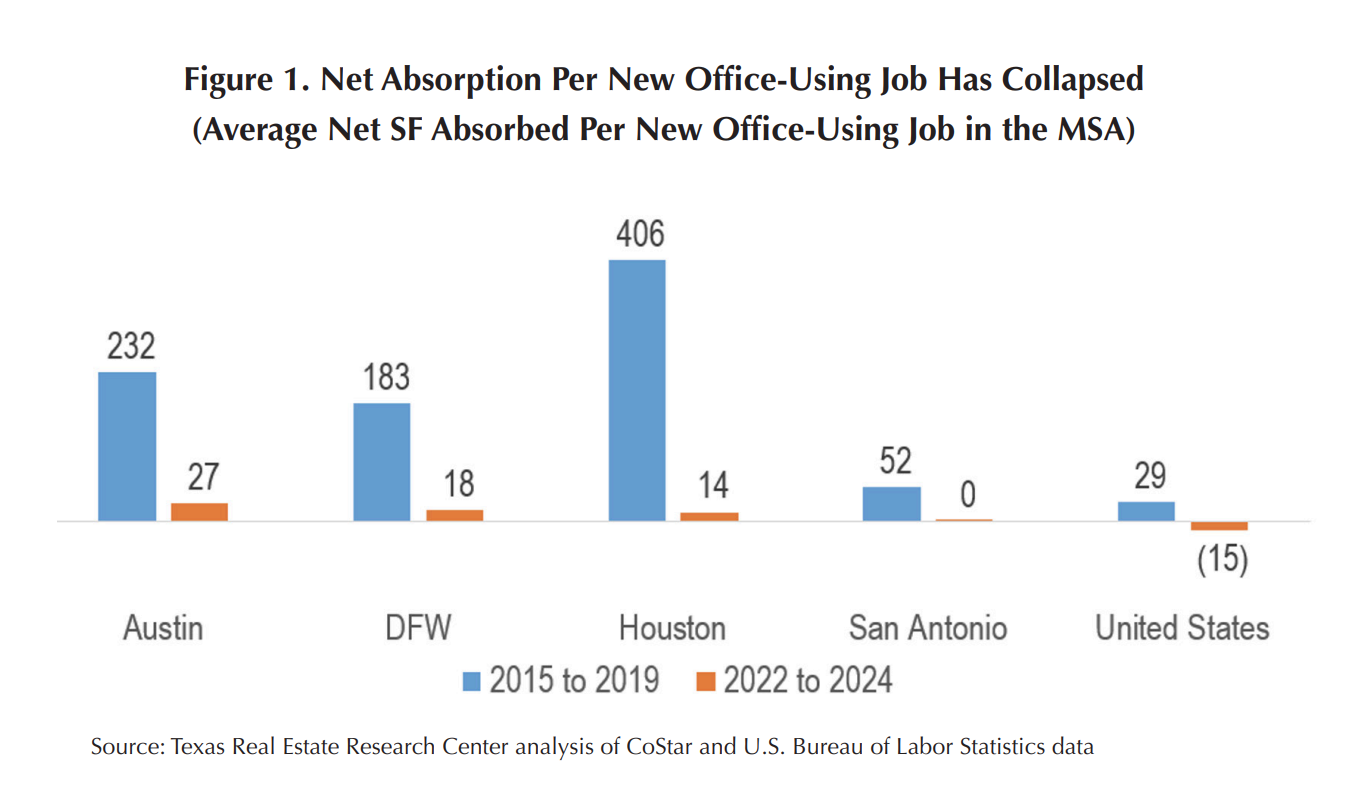

It’s well known that office attendance has been slow to recover since employees were sent home during the lockdown of 2020. Even though Texas’ office-using employment has grown by half a million jobs since then, office use hovers at two-thirds the pre-COVID level, according to Kastle Systems. This employment growth is not translating into significant office absorption (Figure 1). In the good old days, Austin and Dallas tenants added around 200 square feet for each new office-using job in the market. Houston’s energy-rich office economy was even more generous with absorption. Since COVID, all major markets have suffered with much lower absorption from new jobs.

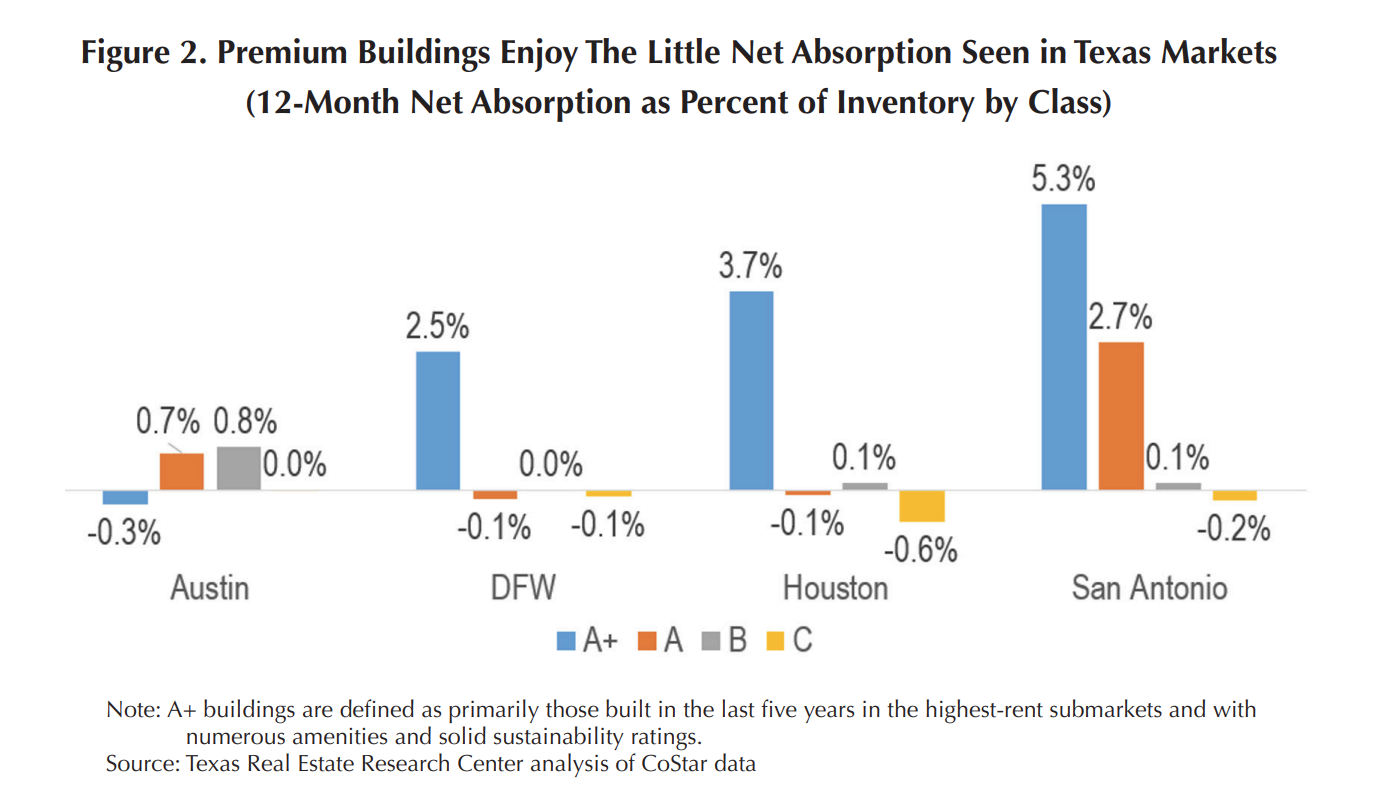

Tenants continue to evaluate their leases in anticipation of future needs. Brokerages and data vendors like CoStar estimate that only half of the leases negotiated before 2020 have come up for renewal, so the full impact of new workplace policies is yet to be seen. While some firms have reduced space, others have taken advantage of owner concessions and added space for growth. (Trends vary. For example, see “The Verdict Is In: Legal Industry Key to Texas Office Markets” on trends in the Texas legal industry.) The net effect of firms’ leasing activity has been felt differently across class. There appears to be a flight to quality, but firms have been much more interested in adding space in the best new buildings (Figure 2). This trend represents the decisions of newly arrived firms and existing firms choosing to relocate.

With ten million square feet of office space delivering in 2024, tenants have ample options. If we segment the office market into four classes, including sorting Class A buildings into the best (A+) and the rest (A), we see that premium building owners in most markets enjoy positive net absorption. Most other classes are flat or losing occupancy.

The financial consequences of this sorting are playing out differently across our major markets (Figure 3). We know asking rents tell an incomplete picture. Anecdotes abound of significant concessions in terms of month’s free rent and generous tenant improvement allowances. Still, asking rents reflect owner expectations and are the only systematic measure available.

With Austin’s generally newer office stock, there is little difference in asking rent growth between class A+ and A buildings. In Dallas, A+ and C buildings have higher rent growth. Much of the city’s older Class A properties from the 1980s oil boom are opulent buildings, but they lack the more efficient and environmentally certified attributes of newer properties.

Class C buildings may be showing rent growth from a combination of boutique firm’s interest in historic properties and a shortage of options in lower-income submarkets. Houston’s office market, with nearly uniform rent growth across class, still seems to suffer from the last energy bust. Its newer buildings lack significant pricing power. San Antonio’s asking rent growth resembles Austin’s, with higher classes enjoying higher growth. In the Alamo City’s case, however, slower but steady job growth and modest office deliveries allow the market to sort out a more normal rent structure.

We are in the midst of an office resorting. Differences in local job growth and industry mix, combined with the unique legacies in each market’s office stock, will influence the outcome. The results will vary by market and even by neighborhood. New buildings in dynamic submarkets will continue to reap prestige tenants. Older Class A and good Class B buildings will stabilize with less choosy occupants. The fate of other buildings will be determined one by one as their (sometimes new) owner evaluates the prospects to renovate vs. convert vs. demolish.

You might also like

TG Magazine

Check out the latest issue of our flagship publication.