Northeast Texas’ crop portfolio is changing. The once attractive corn and soybean market is being impacted by price declines, oversupply, and an uncertain trade environment. Meanwhile, cotton is again becoming attractive to growers thanks to new production ideas such as vertical integration.

Aug 8, 2019

Turning Soil

Northeast Texas Croplands Evolve

It’s basic economics: crop production will always be influenced by supply and demand. For a textbook example, look no further than Northeast Texas, where the crop portfolio is once again changing. The twist? Cotton could make a comeback with the help of some innovative thinking.

For decades, Texas land prices have largely been determined by recreational users or capital investors. Conventional wisdom regarded farmers and ranchers as a peripheral force in land markets. However, they are a vital, if less visible, part of the market. They continue to buy land, especially acreage most suited to raising crops and livestock. The ebb and flow of commodity markets determining which crops producers grow is a dynamic on display in Northeast Texas (Region 4). Now an innovation in cotton production in the region promises to change cropland markets in a broad swath of Texas and surrounding states.

The spike in demand for corn and soybeans throughout the first decade of 2000 had producers introducing corn and soybean production in traditionally less suitable locations. This is especially true for Northeast Texas. The region’s crop portfolio changed from predominantly wheat, sorghum, and cotton to wheat, corn, and soybeans. Today, as the markets for corn and soybeans become riskier, areas with less ideal climates are reverting to more suitable crops.

Northeast Texas’ Changing Crop Portfolio

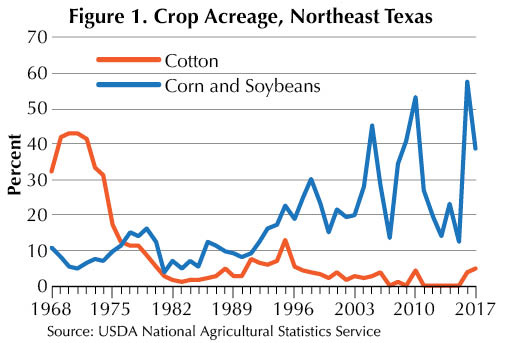

Taking a closer look at nine Northeast Texas counties—Delta, Fannin, Franklin, Hopkins, Hunt, Morris, Lamar, Red River, and Titus—the evolution of the crop portfolio is apparent. Until 1975, cotton was an equally competitive crop in the region, accounting for anywhere from 31 to 43 percent of acres planted. From 1975 to 2000, cotton acreage dropped substantially and averaged 6 percent per year as financial conditions made cotton less profitable. During that time, sorghum took over much of the acreage once dedicated to cotton, likely a result of labor constraints and lower expenses associated with sorghum production.

The rapid loss of gins in the area also increased transportation costs for cotton producers, further incentivizing the move away from cotton production. In addition, wheat came to dominate the region’s crop production, accounting for 65 percent of acres planted since 1980. By 2007, so little cotton was planted there that USDA data showed no acreage dedicated to cotton production for the next decade.

In general, the region’s soil and climate are not optimal for corn and soybeans, especially without adequate irrigation. Therefore, at lower prices, corn and soybeans did not provide sufficient compensation to cover the risk of producing them. However, their prices reached levels too good to ignore in the early 2000s, and the two crops entered the local market as major competitors for acreage.

The introduction of Roundup Ready seed technology in the 1990s enabled farms with minimal labor to produce Roundup Ready corn and soybeans. In 2002, corn and soybean acreage increased considerably from a total of 13 percent to an average of 30 percent. The crops used the second-largest amount of acreage in the region. In 2016, they reached a maximum acreage at 58 percent of acres planted (Figure 1), surpassing the historical contender, wheat.

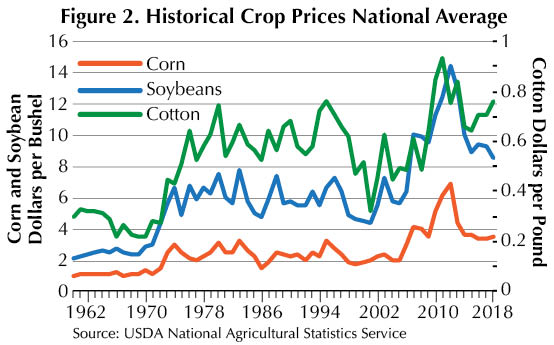

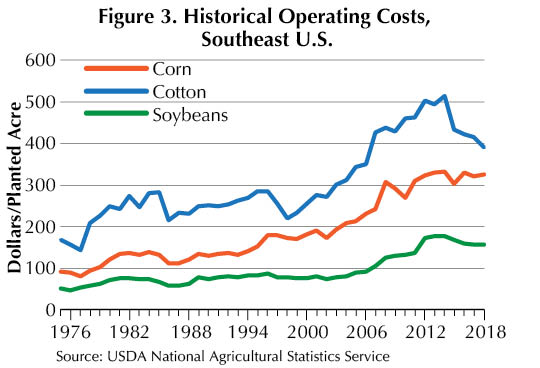

Several fundamental factors pushed the region into corn and soybeans. Corn, cotton, and soybeans all had price declines in the early 2000s, but cotton was hit the hardest with a 24 and 38 percent contraction in 1999 and 2001, respectively (Figure 2). Corn and soybean prices during that time declined more modestly with average decreases of 0 and 4 percent, respectively. Further motivating the switch, cotton operating costs increased 10 percent in 2000 and an additional 8 percent in 2001.

Corn and soybean costs remained relatively unchanged in the three years prior to 2002 (Figure 3). From 2002 to 2017, acres planted for corn and soybeans averaged a third of the acres planted in the region. By 2016, corn and soybeans accounted for nearly 60 percent of the acres planted. Cotton, as noted, went several years with hardly any acres planted.

Recent production numbers hint at a reversion not seen in several decades. Cotton has jumped to 12 percent of production in the region from previously near-zero reported acres. Corn and soybean acreage fell to 35 percent in 2018, contracting 23 percentage points from its high and continuing a negative trend.

Prices for all crops have contracted from their peaks in 2011 and 2012. Corn and soybean prices have declined substantially—by 48 and 40 percent, respectively. Cotton, on the other hand, has contracted only 19 percent. It benefited from positive price movements in 2013, 2016, and 2017. Operating costs for each crop have remained relatively stable, increasing on average 3 to 5 percent annually. The year-over-year changes have evolved generally in the same manner for all crops.

The once attractive corn and soybean market has proven risky given price declines, oversupplied markets, and the uncertain trade environment. The adverse market has producers considering reverting to previous crop portfolios. Reverting to cotton and wheat production, for which the region’s soil and climate are better suited, reduces the growing risk associated with production, and the moderate cost increases and stronger price movements prove promising for producers.

Innovating the Cotton Industry

In addition to these factors, an innovation in cotton production and product marketing could change the face of Texas’ cotton industry. In 2015, a cotton gin offering vertical integration (in which multiple steps of a production process are handled by one business rather than several) became operational in Northeast Texas, boosting local demand for production. PPF Gin in Cooper offers cotton producers a risk-reducing structure and an incentive to go back to cotton production.

PPF owner Pat Pilgrim transferred a model of vertical integration from poultry production to cotton. Pilgrim learned about the efficiencies and improved quality control of vertical integration from his experience at Pilgrim’s Pride working with his father, Bo Pilgrim. The younger Pilgrim realized the opportunity for vertically integrating the cotton-processing method through his own experiences with inefficiencies in delivering cotton for processing.

Pilgrim’s program offers contracted growers a predetermined price for cotton while providing planting seed, fertilizer, other chemical inputs, agronomic consulting, picking/hauling, ginning, and warehousing services. According to Texas A&M AgriLife planning budgets (agecoext.tamu.edu/resources/crop-livestock-budgets/), the most likely (least variable) of these input costs represents at least 50 percent of total cotton production costs traditionally paid by farmers. This represents a substantial sharing of the financial risk of cotton production. Pilgrim also selects the cotton variety planted each season, focusing on the needs of the end product.

The majority of the cotton PPF processes comes from about a 100-mile radius around the gin, but some growers farm as far south as Austin, as far north as Tulsa, and even in Arkansas. PPF employs 60 people and can process 1,100 bales per day. It also has a storage capacity of about 90,000 bales of processed cotton.

Pilgrim has no doubt the presence of the gin has encouraged producers to return to cotton. He has seen the number of cotton acres increase substantially. Pilgrim plans to increase the gin’s capacity by about 10 percent per year. Eventually, he will spin thread and produce consumable products such as cotton swabs, cotton balls, and towels. Cotton has for some time been largely an export commodity. Pilgrim believes consumers’ demand to know where their products are grown and made has created a market for processing cotton domestically. This demand may keep cotton production in the region.

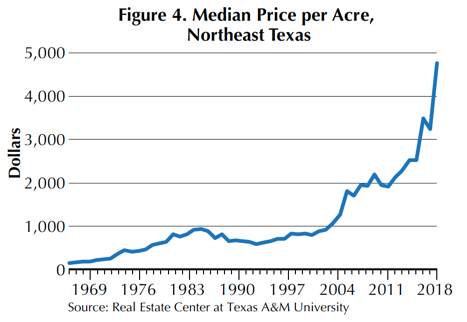

Reflecting these agricultural production realities, land markets in the nine counties studied showed increased volatility in price and volume beginning in the 2000s (Figures 4 and 5). Although the region is heavily influenced by recreational land purchases from nearby metropolitan areas, those purchases are characterized by smaller acreage sold at higher per-acre values.

Agriculturally inspired demand has historically set a floor for land prices. Typically, reduced risk leads to higher average profits. If the integrated marketing approach succeeds for cotton in northeast Texas, participating producers should see a more stable and profitable bottom line. In turn, that would allow them to pay more for farmland, perhaps boosting prices and activity in that market and raising the land-price floor.

____________________

Dr. Kiella ([email protected]) is an assistant research economist with the Real Estate Center at Texas A&M University, Dr. Robinson ([email protected]) is a professor and extension economist with the Department of Agricultural Economics at Texas A&M University, and Dr. Gilliland ([email protected]) is a research economist with the Real Estate Center at Texas A&M University.

Did you like this Article?

You might also like

6 minute read

May 30 2018

Magnificent Seven

Texas Land Market Regions

In 2002, the Real Estate Center embarked on the challenge of dividing roughly 268,600 square miles of varying Texas landscapes into distinct regions, each with a unique set of soil and land-use types. The result? More accurate reporting of land market trends.