- Food and beverage manufacturing is a growing industry with much economic potential.

- Investment is on the rise.

- Perishable raw materials need specialized places and workers with specific skills.

- Bakeries, snack food manufacturers, and beverage plants are examples of providers that locate in major markets.

Apr 22, 2024

Bake to the Future

Texas Food and Beverage Manufacturing

The state’s burgeoning food and beverage manufacturing industry has much more potential for the Texas economy, and we don’t just mean Blue Bell and Whataburger.

More than 128,000 Texans earn their daily bread manufacturing food for the rest of the state. While the industry is already important and growing, there’s room for more local investment. That’s essential for jobs, real estate, and the lives of Texans.

The food-manufacturing industry is different from other goods-producing industries. The raw material is perishable. Food is also essential, and this attracts a lot of attention. The industry is heavily scrutinized from cultural, health and nutrition, and even national security perspectives. These distinctions impact site selection and operations in important ways.

An Industry with a Unique Flavor

Food spoils quickly, adding cost and complexity to the industry. Extraordinary efforts go into moving products from farm and feedlot to consumers quickly. Factories, warehouses, trucks, and rail cars that serve the industry must have refrigeration and freezer capacity, and workers with specialized skills are needed to maintain the air conditioners and freezers. Running and maintaining specialized equipment to quickly process, preserve, and package food adds further to the industry’s talent burden. Food-manufacturing facilities tend toward hot and cold climate extremes and can be messy environments. This means the industry pays a premium for production talent at every skill level.

Such manufacturers balance access to suppliers and access to customers when siting facilities. With enough capital investment, most any food can be grown anywhere. In practice, it is often cheaper to source various crops and animals from where nature favors them. In these cases, initial processing tends to locate near the source. Examples include grain milling, animal and seafood processing, and winemaking. Once processed, the intermediate products can be shipped elsewhere for consumption or as ingredients in higher value-added products. These secondary facilities have the flexibility to locate closer to consumers. Bakeries, snack food manufacturers, and beverage plants are examples of providers that locate in major markets. These economies mean some food-processing activities are more concentrated than others. This, in turn, influences the talent and facilities needed in each local market.

The importance of food makes it highly political. Because of the health risks that accompany improperly processed food, the industry is heavily regulated. Federal farm legislation, in the form of price supports and other incentives, influences the costs faced by food manufacturers.

In addition, food is a matter of national security, grouped with other sectors such as pharmaceuticals and semiconductors as having critical strategic importance. The COVID pandemic demonstrated the risks from the failure in the food supply chains.

And, of course, food manufacturing is strongly influenced by consumer preferences. Food is intimately associated with culture, health, and lifestyle, so manufacturers must deal with changing interests and tastes. Important examples include attitudes on environmental stewardship, farm worker and animal welfare, or genetically modified crops and animals. Markets are impacted by growing cultural diversity and interest in cooking and new cuisines.

Measuring Industry Growth

Food manufacturing may be assessed in several ways, including by payroll employment, business establishments, and capital investment. Nationally in 2023, 2.1 million people worked in food and beverage manufacturing, accounting for 16 percent of all manufacturing jobs. The nearly 130,000 Texas food and beverage jobs account for a smaller share of state manufacturing jobs (13 percent).

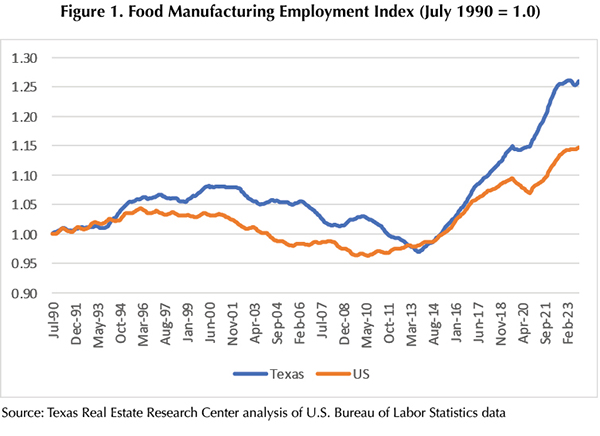

After a period of flat employment, food manufacturing has grown dramatically (Figure 1). Except for a temporary reverse during the COVID pandemic, the industry has been on a ten-year uptrend. Texas employment outpaced the nation with over double the national increase in the last five years (15 percent versus 6 percent, respectively).

In the last five years, food and beverage manufacturing employment also exceeded the change in overall employment. Nationally, employment grew by 4.9 percent while food and beverage employment grew by 7.9 percent. In Texas, the five-year increase in food and beverage was 14.9 percent compared with total job growth of 11.5 percent.

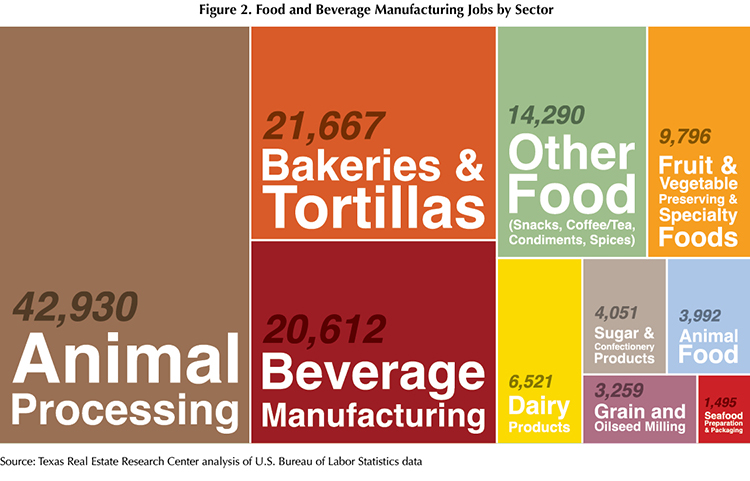

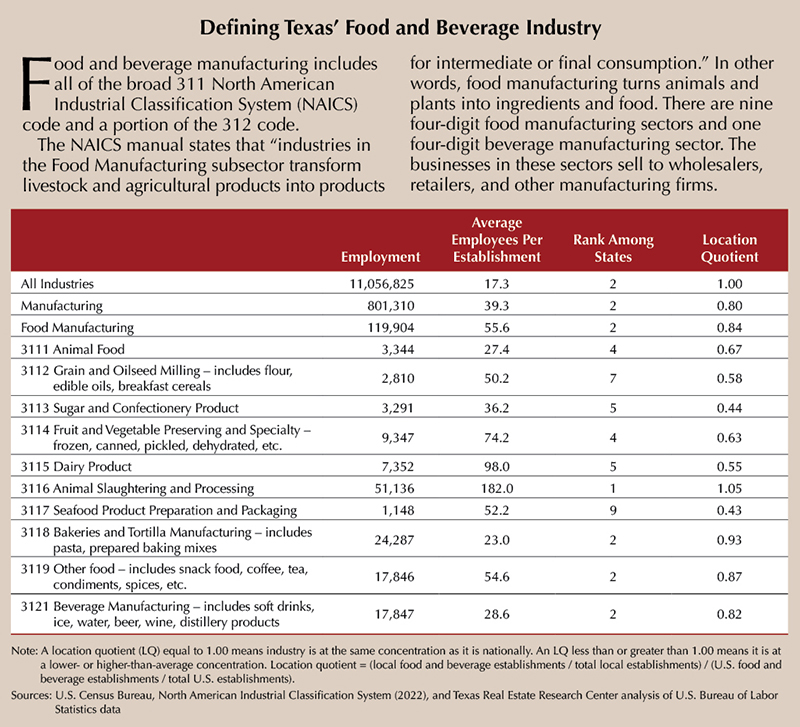

In Texas, most food jobs are in three subsectors: animal processing, beverages, and bakeries and tortilla manufacturing (Figure 2). Almost 43,000 Texans work in animal slaughtering and processing. Nearly 22,000 bake, and an additional 20,000 produce beverages.

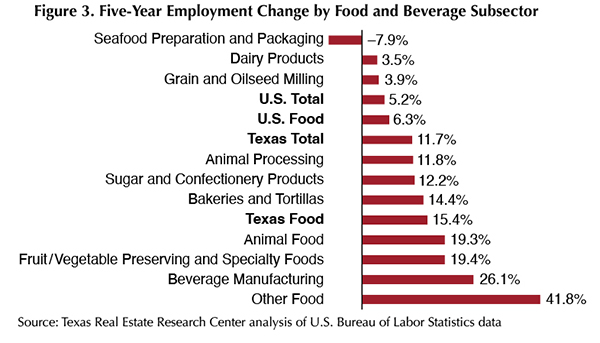

Five-year growth rates in the subsectors range from an 8 percent job loss in seafood processing to a whopping 42 percent increase in the “other food” category (Figure 3). Beverage employment growth came in at a strong 26 percent. Most sectors in Texas have been adding jobs faster than the overall Texas economy. Seafood, grain and oilseed milling, and dairy products were the only sectors that didn’t see rapid growth.

Business establishments are another helpful way to measure the industry. The federal government collects data annually on establishments that are defined as a stand-alone business operation. Tracking establishments helps assess real estate demand since, just as households are the demographic unit that occupies a residence, establishments are the economic unit that occupies commercial space.

Across the U.S., the five-year change in total employment, total manufacturing, and food-and-beverage-manufacturing establishments was 5, -2.9, and 15.9 percent, respectively, according to the most recently available data, which were from 2021. In Texas, the comparable changes were all positive and higher than their national counterparts at 10.2, 3.8, and 23.5 percent, respectively.

Food and beverage manufacturing has seen robust growth, beating overall manufacturing by nearly 20 percent at the state and national levels.

Industry Investment Rising

In the five years ending in 2022, food-manufacturing firms made almost $350 billion in investments in productive assets (facilities, equipment, etc.). Over those five years, the annual level of investment increased by 39 percent, exceeding the 27 percent change in investment for manufacturing overall. Investment in food-manufacturing structures alone grew even faster than the total capital investment rate. Over five years, the increase in food and beverage manufacturing was 70 percent, compared with a 57 percent increase in overall manufacturing.

Investment in specialized food processing and refrigerated space has also grown. In Texas, 4.4 million square feet of such space was added in the last two and a half years according to Costar. This space had a 7.7 percent vacancy rate and saw rents at $8.25 in 4Q2023. Rent rates were in the double digits in the waning quarters of the pandemic.

Texas is indeed a powerhouse food manufacturer, ranking second among states in most food subsectors (see sidebar). However, Texas does not have an exceptionally high concentration of food manufacturing. The location quotient for most subsectors is less than the national average of 1.00. Some of these deficits are due to a lack of local availability of necessary crops or animals, but there are opportunities to expand some subsectors. Facilities that process secondary and higher value-added products such as animal food, confections, and other foods and beverages can be sited almost anywhere, and these all have lower-than-average concentrations in the state.

Food Manufacturing Across Texas Metros

Food manufacturing plays a role in every Texas metro’s economy, and a substantial one in some. The larger markets host the most establishments. The Metroplex is home to 24 percent of all establishments, followed by Houston (20 percent), Austin (11 percent), and San Antonio (8 percent).

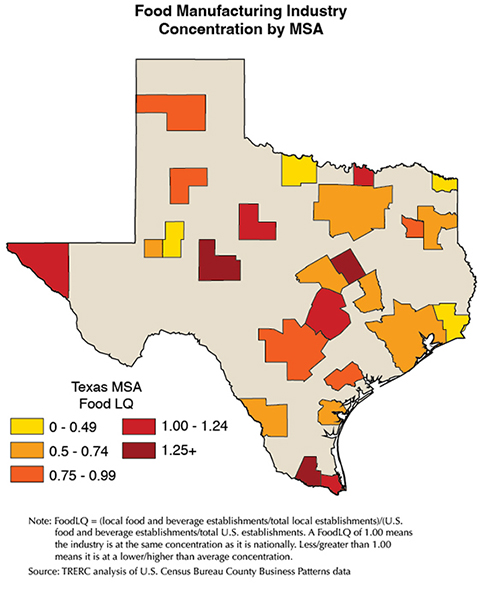

When considering the concentration of establishments, a different picture emerges. Food and beverage manufacturing is most heavily concentrated in San Angelo, Waco, Sherman, and the two Rio Grande Valley metro areas of McAllen and Brownsville (see map and table). Of the Big Four metros, only Austin has a higher-than-average concentration, at a modest 1.02. This means the industry is underrepresented in many Texas cities. These deficits represent important economic development opportunities, especially with Texas’ rapid growth.

Hungry for Growth

Food and beverage manufacturing is an important and growing industry with much more potential for the Texas economy. Continued population growth will no doubt motivate more investment by this industry in the state. Those businesses will need specialized spaces and workers with specific skills.

Real estate and workforce stakeholder support will be needed to boost the industry. Any enhancements to Texas’ agricultural sectors, including farms, fisheries, orchards, and ranches, can only help attract more interest.

____________________

Daniel Oney, Ph.D. ([email protected]) is research director with the Texas Real Estate Research Center.

Did you like this Article?