Land Insights | Fall 2024

“Mixed” was the byword for the first quarter of this year when it came to land prices and sales volume declines across the state. This is true for the second quarter as well.

Editor’s note: The data in this article were current at the time of author’s submission on August 12, 2024.

Texas Large Rural Land Market Overview

“Mixed” was the byword for the first quarter of this year when it came to land prices and sales volume declines across the state. This is true for the second quarter as well; however, prices are more uniform than in the prior quarter, with rates of increase slowing in some regions and rebounding in others.

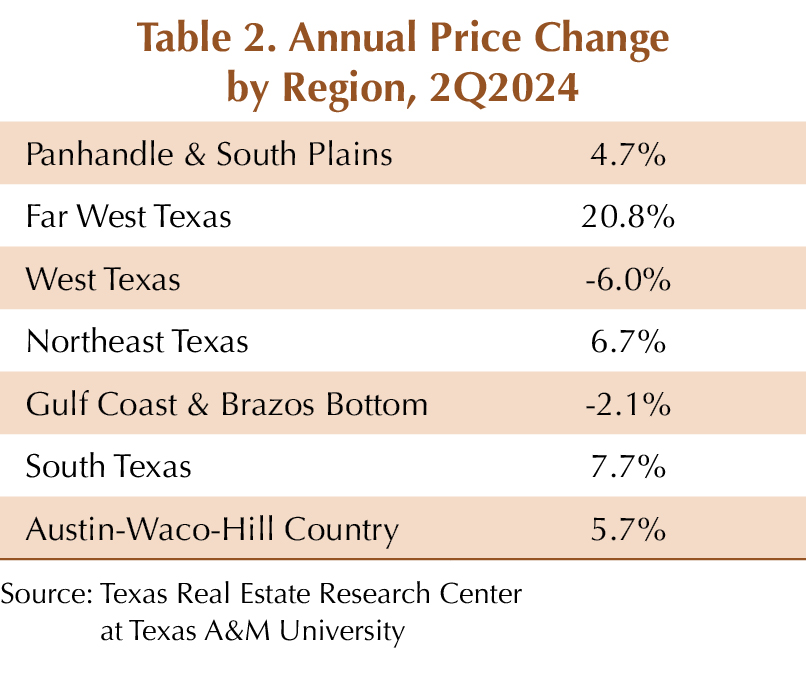

Prices bounced back a bit in Region 1 (Panhandle & South Plains), slipped in Region 3 (West Texas), slowed in Region 4 (Northeast Texas), and turned from negative to a new high (at least temporarily) in Region 7 (Austin-Waco-Hill Country). Two things remained the same on a year-over-year (YOY) basis: the two regions with the best price growth (Northeast and South) saw the largest declines in quarterly sales volumes, while the two regions with negative price changes (West and Gulf Coast & Brazos Bottom) saw some of the smallest declines in annualized sales volumes.

Market Metrics

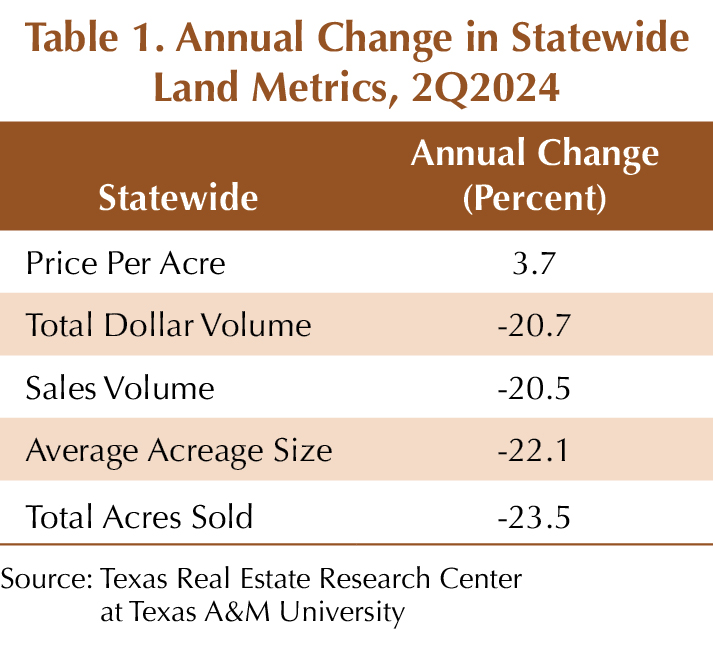

Statewide, the decline in annualized sales volume has eased (Table 1). It is still down YOY, but the rate of decline has dropped from around 45 percent a year ago to about 20 percent through the second quarter. This tapering is good, but hopefully the decline is near an end, because one must go back to 2Q2013 to see total sales this low.

The typical tract size retracted from the same quarter a year ago, down by 22.1 percent, but was up in Regions 1, 3, and 5. Total acres sold statewide was down 23.5 percent. Every region saw a decline in total acres sold, but Region 3 declined only 2.9 percent. Statewide total dollar volume declined by 20.7 percent over the prior annualized total.

Median price continued to rise through the second quarter, increasing 3.7 percent YOY to $4,702. The five-year compound annual growth rate (CAGR) was nearly constant around 10.5 percent across 2023. It slipped to 10.3 percent in 1Q2024 and currently sits at 9.9 percent.

While first-quarter prices were down in four of the seven regions (Table 2), second-quarter prices were down in only two (Regions 3 and 5). Of the 33 Land Market Areas (LMAs), 15 had negative price changes and 16 were positive. Only two of the negative price changes and one of the positive price changes indicated a statistically verifiable trend. The mixture of positive and negative results with few statistically significant shifts suggests a market searching for a sustainable price trend. It will be interesting to see if these prices hold up next quarter, as a continuation of low market activity is expected.

Overview and Outlook

Current financial circumstances and uncertainty about future economic conditions continue to subdue market activity. Contributing factors include constrained liquidity, declining personal net savings, domestic political uncertainty, and growing geopolitical risks. Consumer debt, including credit card debt, continues to rise, while aggregate personal savings is now well below 2019 levels. Another concern is the unprecedented rise in government debt accumulation. Meanwhile, recent national employment reports show signs of weakness.

Rural land markets are holding up well under the circumstances. Activity seems to be leveling off, and some regions show slight improvements in recent quarters. However, the lack of statistically significant shifts can indicate that prices of some categories of land are falling while others are increasing.

Our latest forecast model indicates statewide price per acre is likely to hold at current levels over the next two to three quarters and then begin to gradually decline about 5 percent by the end of 2025. However, it predicts total acres sold should reach a floor by year-end and then begin to gradually rise through 2025 and beyond. Like any forecast in a dynamic market, several factors could change unexpectedly and alter these predictions by next quarter.

Uncertainty in capital markets, specifically potential interest rate changes and recession fears, seem to be rumbling over investment activity like storm clouds. Nonetheless, savvy investors usually act before the clouds clear. Some are making moves and, most likely, many more are evaluating near-term opportunities.

____________________

Lynn D. Krebs, Ph.D. ([email protected]) is a research economist with the Texas Real Estate Research Center.