A recent Texas Real Estate Research Center study found low-income households were less likely to have homeowner’s insurance than higher-income households, both in metropolitan and nonmetropolitan areas. This is also true among homeowners who do not have a mortgage.

Jun 28, 2021

Storm Warning

Winter Blast a Harsh Reminder of Need for Homeowner's Insurance

First an unprecedented winter storm, and now hurricane season. Make no mistake: Texans are weather weary. That goes double for uninsured homeowners, and there are more of those than you might expect.

In February 2021, Winter Storm Uri caused temperatures to fall overnight into single digits and lower across much of Texas, resulting in an estimated $130 billion in damage and economic losses and more than 150 deaths. If the estimates are correct, Uri is one of the costliest weather disasters in the state’s recent history.

It also accentuated the importance of having homeowner’s insurance. Many homes were in need of repairs from damage caused by the snow and ice. Households with homeowner’s insurance avoided a major financial hit. Those without insurance, on the other hand, were faced with paying the full repair bill out of pocket.

Identifying the location and characteristics of uninsured homeowners would enable the state to better allocate resources for home repairs following a natural disaster such as a freeze. To that end, the Texas Real Estate Research Center used the U.S. Census Bureau’s 2019 Integrated Public Use Microdata Series (IPUMS) to estimate the number of uninsured households in Texas. The sample data sets include single-family attached and detached homes. Households that self-reported no property insurance payment were considered uninsured.

Comparison by Metro

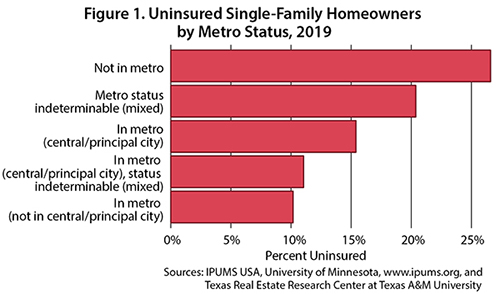

The Center found nonmetro homeowners were more likely to be uninsured than metro homeowners (Figure 1). Approximately 26.6 percent of nonmetro homeowners reported as uninsured compared with 11 percent in metropolitan areas in a central/principal city (Austin, Dallas-Fort Worth, Houston, and San Antonio) and 10.2 percent in metropolitan areas not in a central/principal city (rest of Texas’ Metropolitan Statistical Areas).

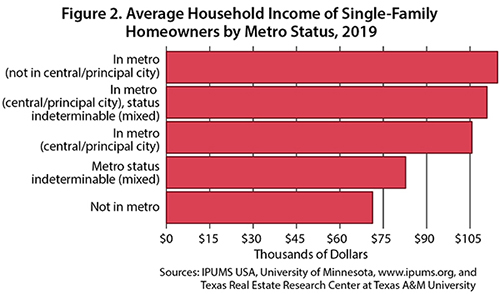

In addition, the Center’s analysis incorporated average household income by metro status and found a relationship between being uninsured, having a lower household income, and living in a nonmetro area. Metropolitan areas had a higher average household income than nonmetropolitan areas (Figure 2), registering above $100,000 for both in and not in a central/principal city compared with $71,326 for a nonmetro household.

Metropolitan areas in the Rio Grande Valley and along the Texas coast record the highest percentages of uninsured households (Figure 3). McAllen leads at around 37.5 percent, with almost two out of five households uninsured. Brownsville follows close behind with 34.9 percent. Despite being vulnerable to hurricane damage for decades, Beaumont and Corpus Christi register relatively high levels of uninsured homes—21.5 and 19.8 percent, respectively. In other words, one out of five homeowner households there is uninsured.

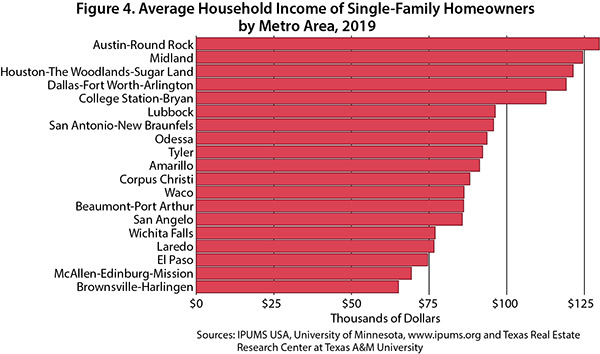

In contrast, the smallest percentages of uninsured households are in Austin and Dallas-Fort Worth with 6.1 and 7.4 percent, respectively. As before, the study found a relationship between lower income levels and uninsured households in the metropolitan areas (Figure 4).

Mortgage Status and Insurance Coverage

Mortgage status plays an important role in determining the likelihood of having property insurance given that mortgage contracts require a homeowner’s insurance policy. The mortgage lender has a potential financial interest in the home, which is the motive for requiring insurance.

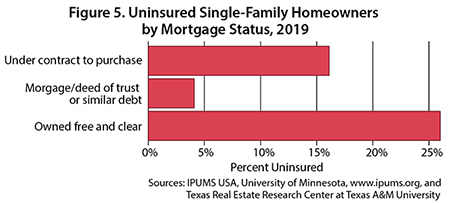

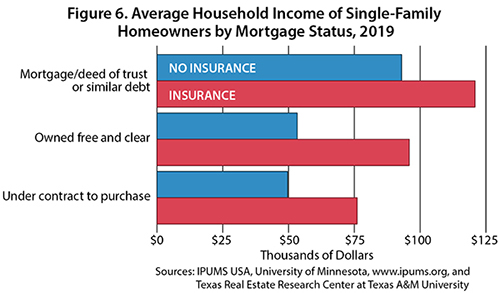

Only 4.1 percent of homeowner households with a mortgage are uninsured compared with 26 percent who own their home free and clear of debt (Figure 5). It’s possible that mortgagors without insurance could have unconventional or mortgage-like debt structures rather than more ubiquitous conventional mortgages.

Once again, a relationship is found between having lower average household incomes and being uninsured. Those who own their home free and clear of debt and are uninsured have an income of around $53,274 compared with $95,873 for those who own their home and are insured (Figure 6).

Homeowners who don’t have a mortgage are generally characterized as seniors living in older homes that are more susceptible to damage from extreme weather conditions.

Winter Storm Uri was a harsh reminder of the importance of having homeowner’s insurance, but it’s hardly the first. A surprisingly high percentage of homeowners in the Gulf region are uninsured, living under the threat of hurricanes year after year. Many have suffered home damage as a result.

When one considers the link between household income levels and being uninsured, this raises important questions. Is homeowner’s insurance too expensive for households earning a lower income? Is the cost impeding them from protecting their homes from natural disasters?

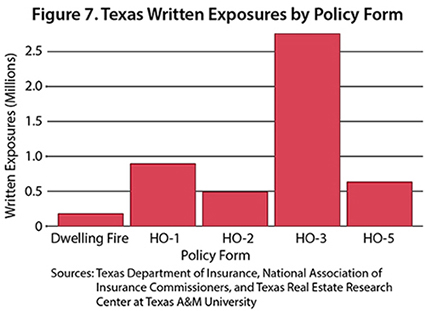

This study used 2019 data from the National Association of Insurance Commissioners via the Texas Department of Insurance to analyze Texas homeowner policies. Data are for owner-occupied properties with one to four dwelling units.

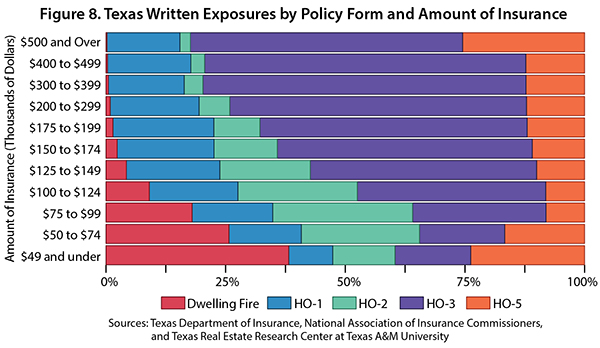

The amount insured is based on the cost-based value of the insured property. Most policies in Texas are “H0-3,” which generally provides higher coverage for disasters (Figure 7). This indicates homeowner households that have property insurance would probably be protected by the damage caused by Winter Storm Uri. Coverage can vary among policies where lower (higher) valued homes tend to have less (more) coverage (Figure 8).

____________________

Dr. Torres ([email protected]) is a research economist and Roberson ([email protected]) a senior data analyst with the Texas Real Estate Research Center at Texas A&M University.

Did you like this Article?

You might also like

7 minute read

Sep 06 2018

Highs & Lows of Floodplain Regulations

Houston has adopted new building regulations intended to protect homes in the city’s most flood-prone areas. The regulations will increase new-home construction costs, but they could also have human and economic benefits. Whether those benefits will outweigh the cost increases is the big unknown.

Single-family

10 minute read

Mar 25 2024

How Natural Disasters Affect Homebuying Decisions

The combination of climate change and economic growth in disaster-prone regions increasingly exposes Texas’ population to extreme weather events (IPCC, 2023). Natural disasters have an immediate impact on economic activity and typically lead to net out-migration, decreased income, and lower real estate values (Boustan et al., 2020).