Are REITs On the Mend?

The Federal Reserve’s most recent interest rate hikes have had a negative impact on the real estate investment trust (REIT) sector. But with the Fed signaling that it will soon begin to lower rates, could it be time for a turnaround?

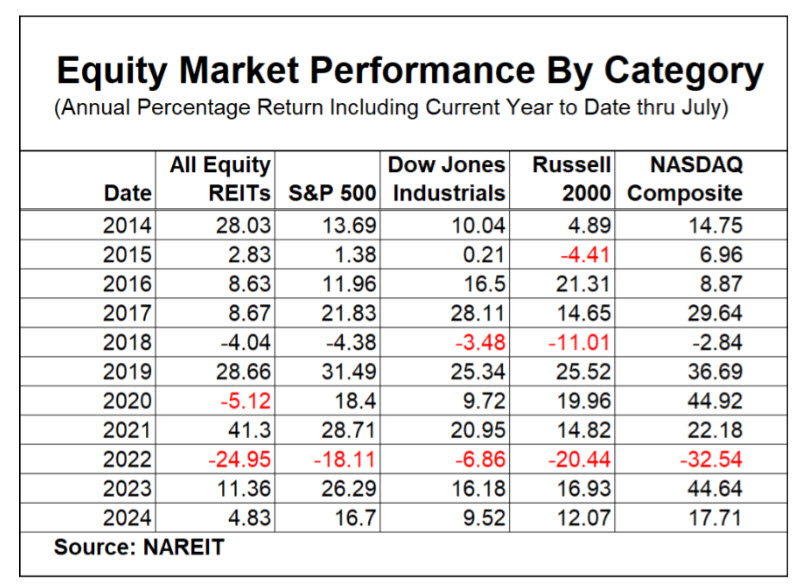

The Federal Reserve’s most recent interest rate hikes have had a negative impact on the real estate investment trust (REIT) sector. Statista reports that there were 195 U.S. REITs in 2023, significantly lower than the 2015 peak of 233. Higher interest rates have resulted in a higher cost of borrowing for REITs, hurting their performance for the last two years compared to other equity investments (see table). But with the Fed signaling it will soon begin lowering rates, could it be time for a turnaround?

The National Association of Real Estate Investment Trusts (NAREIT) defines REITs as companies that own, operate, or finance income-producing real estate across various property sectors. REITs offer investors the opportunity to invest in income-producing real estate without directly owning or managing properties themselves. Types of REITS include:

- Equity REITs: Own and operate income-producing real estate.

- Mortgage REITs: Provide financing for real estate by purchasing or originating mortgages and mortgage-backed securities.

- Public REITs: Traded on major stock exchanges.

- Non-listed REITs: Registered with the SEC but not traded on public exchanges.

- Private REITs: Neither registered with the SEC nor traded publicly.

According to S&P Global, merger and acquisition (M&A) activity involving public U.S. equity REITs was quite low in 2024, with only a single deal announced in the first half of the year. Increases in interest rates have driven the cost of debt higher, resulting in the lack of REIT transactions.

Morningstar reports that the REIT sector has underperformed the broader stock market. Over the past year, the Morningstar US Real Estate Index returned 7.25 percent while the Morningstar US Market Index returned a much larger 26.4 percent. The consensus thinking is that the underperformance is primarily due to the REIT sector’s interest rate sensitivity.

Many REITs are still trading at large discounts to their estimates of net asset value (NAV). S&P Global reports that within the REIT sector, hotel, office, and timber REITs trade at the largest discounts to NAV. It may be worth monitoring REITs trading at a discount since they may become attractive M&A targets in the future, increasing their value.

Conversely, areas where REITs are trading at the largest premium are in the healthcare and datacenter sectors according to S&P Global. Retail shopping center REITs also bear watching, as they may benefit from changes in consumer behavior and tight brick-and-mortar supply.

Although there could still be challenges ahead, I am cautiously optimistic about the REIT sector. If interest rates do begin to decline and commercial real estate transactions move up to a more normal range, the sector could see significant improvement. This is not an advocation for going out and investing in REITS today. However, favorable dynamics may be ahead for those REITs with strong fundamentals and solid long-term expectations for rent growth.

Folks interested in the sector should note that there are liquidity and disclosure requirement differences between publicly traded REITs, public non-traded REITs, and private REITs. These differences should be studied carefully.

You might also like

TG Magazine

Check out the latest issue of our flagship publication.