An annual increase of $1 in homeowners’ costs (tax, insurance and maintenance, for example) can be expected to decrease home value by $16.50, according to a study conducted by the Real Estate Center.

Jul 3, 2014

Rising Flood Insurance, Sinking Home Values

Flood insurance premiums are rising thanks to federal legislation requiring them to reflect actual flood risk. A Center study shows that increases in insurance and other housing costs ultimately reduce home values.

Since the U.S. Congress passed the Biggert-Waters Flood Insurance Reform Act of 2012, the Real Estate Center has received a number of queries regarding the impact of higher flood insurance costs on home values. The act requires the Federal Emergency Management Agency and other agencies to implement a number of changes in the National Flood Insurance Program (NFIP) and requires the NFIP to raise rates to reflect true flood risks. For more information about the Biggert-Waters Flood Insurance Reform Act, see “On the Water Front,” Tierra Grande, April 2014.

The impact of higher home insurance costs on home values is especially relevant to Texas homeowners because home insurance costs here are much higher than national averages (Table 1). A research study at the Real Estate Center on the impact of housing costs on home values in Texas found that a $1 increase in annual owners’ costs (tax, insurance, maintenance) is expected to decrease owner-occupied home values by about $16.50.

Home Values

In a competitive market, the price of a house as an asset is equal to the present value of net rent, just as a company’s stock price is equal to the present value of the future dividends. Home values can be influenced by two major factors: net rent and the investor’s required rate of return. Net rent is equal to gross rent minus property taxes, insurance and maintenance costs. Because the economic life of a house is normally more than 50 years, an increase in annual rent by $1 results in $50 when rents are added up over 50 years. Similarly, an increase in insurance premiums by $1 results in a $50 increase in insurance costs over the life of a house.

In the real world, $1 earned or spent today is more valuable than $1 to be earned or spent a year from now or in later periods because of the potential earning capacity of money. One dollar today is preferred over $1 later. Inflation erodes the purchasing power of money, which means $1 today can buy more goods and services than $1 next year. Future net rents need to be adjusted for the time value of money by multiplying net rents in each period by a discount factor reflecting the time value of money. Because house prices are discounted values of future net rents (and net rents are gross rents minus costs) an increase in housing costs results in a decrease in home values. The decrease in home values is equal to the present value of additional annual costs.

Higher homeowners’ insurance costs are expected to have a negative impact on home values because these costs reduce net rents over the economic life of a home. As it is, Texas homeowners’ insurance premiums have been over 73 percent higher than the national average since 2000 (Table 1).

Metro Housing Costs, Home Values

Housing costs increase with home values. Homes with higher prices have higher property taxes, insurance and maintenance costs. Housing costs as a percentage of home values is an appropriate measure of these costs.

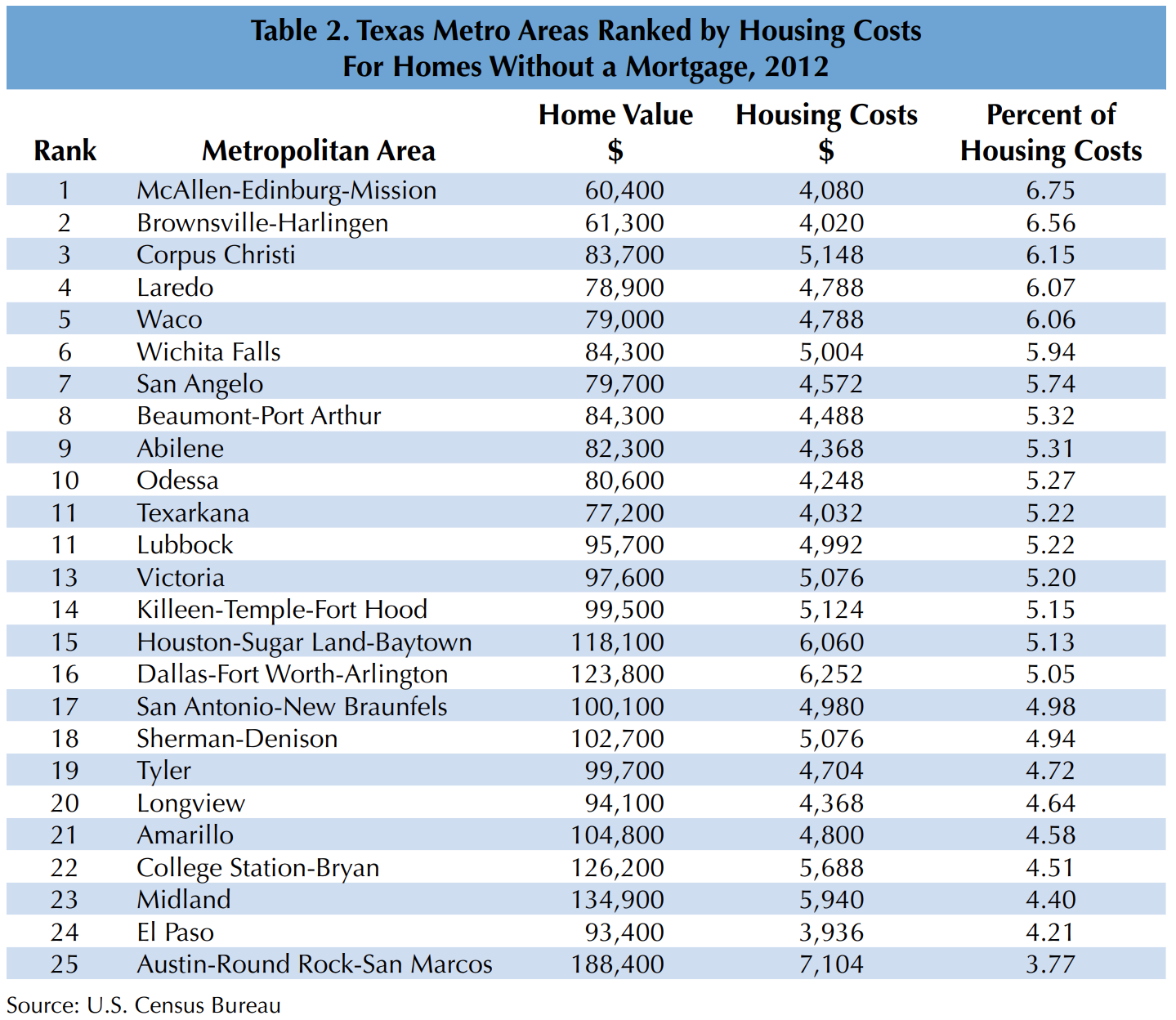

To analyze the relationship between home values and housing costs, the Center compared home values and housing costs of homes without a mortgage. The financing methods used to purchase homes (cash or credit) have no impact on home values. Texas metropolitan areas are ranked by housing cost as a percentage of housing values in 2012 for homes without a mortgage in Table 2. McAllen-Edinburg Mission has the highest cost (6.75 percent) followed by Brownsville-Harlingen (6.56 percent), Corpus Christi (6.15 percent), Laredo (6.07 percent) and Waco (6.06 percent). Austin-Round-Rock-San Marcos had the smallest percentage of housing costs (3.77 percent) in 2012 followed by El Paso (4.21 percent), Midland (4.40 percent), College Station-Bryan (4.51 percent), and Amarillo (4.58 percent).

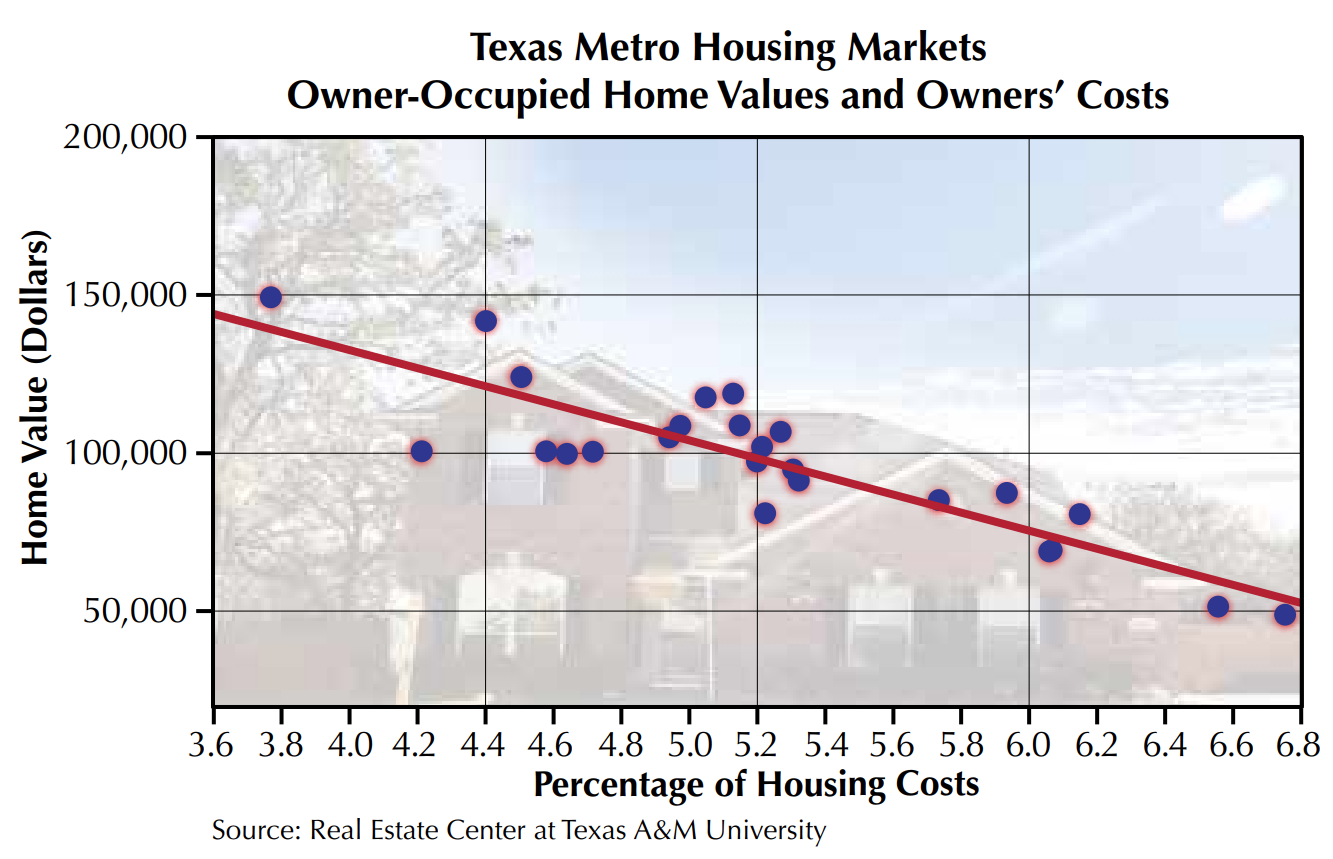

The relationship between Texas metropolitan home values and percentages of housing costs are illustrated in a scatter diagram (see figure). The computed trend line shows a significantly negative relationship between home values and percentages of housing costs; that is, as the percentage of housing costs increases, home prices decline. A regression analysis of the relationships between home values, homeowners’ incomes and percentages of housing costs show that a $1,000 increase in annual housing costs is expected to decrease home values by about $16,500. (Assuming the useful life of a house to be 40 years, the $16,500 decrease in home values is the present value of the increase in annual housing costs over a period of 40 years by $1,000 per annum when the discount rate is 5.3 percent.) So if a homeowner’s flood insurance premium goes up by $1,000 per year, it would on average decrease the value of the average home $16,500.

Some Caveats

There are some caveats about using this study for the analysis of the impact of higher flood insurance costs on Texas home values. First, data for home values and home costs are averages while waterfront home values are normally higher than averages. Second, waterfront homes do not constitute a large proportion of homes in Texas. Third, the passage of the Biggert-Waters Flood Insurance Reform Act of 2012 is expected to have an impact on residential location decisions by Texas homeowners and builders. Because of the flexibility of the supply side of Texas residential markets, Texas builders and Texas waterfront home lovers may be able to optimize the trade-off between the utility of waterfront homes and their higher costs.

Dr. Anari ([email protected]) is a research economist with the Real Estate Center at Texas A&M University.

Did you like this Article?

You might also like

Land Markets

6 minute read

Apr 03 2014

On the Water Front: Flood Insurance Reform Means Higher Premiums

Legislation aimed at tackling the National Flood Insurance Program’s $24 billion debt will end subsidies for nearly 440,000 program participants and base premiums strictly on a property’s risk levels.